Refined nickel price gets a boost

GAVIN WENDT: Here’s some positive supply-side news that’s set to boost the price of refined nickel

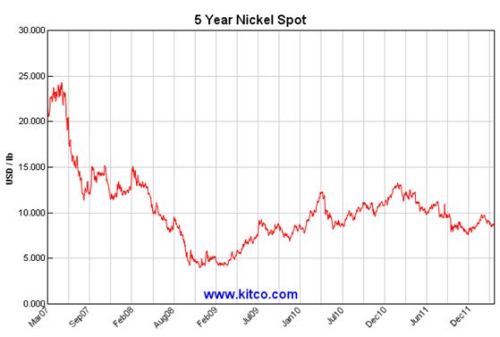

The past few years have been pretty tough ones for nickel, as the five-year price chart below attests.

The price has endured some fairly nasty headwinds, both in terms of a fluctuating demand side and also a burgeoning supply side in the form of cheap Asian pig nickel.

Since the Global Financial Crisis the nickel price has firmed, but not nearly to the same extent as many other commodities.

Nickel was actually the second-worst performing metal on the London Metals Exchange during the second half of 2011.

Nickel slumped by more than 40 per cent during the second half of 2011, making it cheaper than pig iron, a substitute made from low-grade ore typically from Indonesia and The Philippines.

However, this looks set to change, with a major potential game-changer announced recently that could significantly cut nickel supplies and hence bolster nickel prices.

Indonesia has advised that it is bringing forward by two years its ban on nickel ore exports.

A recent Bloomberg News report proclaimed that nickel-ore and bauxite shipments from Indonesia, the top supplier to China, could plunge by 75 per cent during 2012 as a consequence of a ban on metal-ore sales that comes into force during May, two years earlier than scheduled.

Indonesia is a major nickel supplier, so this is big news.

Indonesia shipped 33 million metric tons of nickel ore during 2011 (up from 4 million tons in 2008) and 40 million tons of bauxite during 2011 (up from just 8 million tons in 2008), according to data provided by the Indonesian Mining Association.

It was this surge in Indonesian exports of these raw commodities that prompted the government to advance the ban on companies that hold mining business licenses for production operations.

The government effectively wants to see more value-adding, instead of exports of pure raw materials.

Indonesia is the major supplier to China, so any impact on supplies is likely to have a very positive impact on nickel prices.

Data shows that China buys around 80 per cent of Indonesia’s bauxite imports and 53 per cent of its nickel-ore purchases.

Declining shipments from Indonesia is likely to generate increased competition for supplies amongst Chinese processors – potentially benefiting nickel-ore mining companies elsewhere, like those in Australia for example, as prices are likely to rise.

The move is also likely to increase China’s demand for refined nickel as a substitute for nickel-pig iron, which is positive for traditional Australian nickel companies.

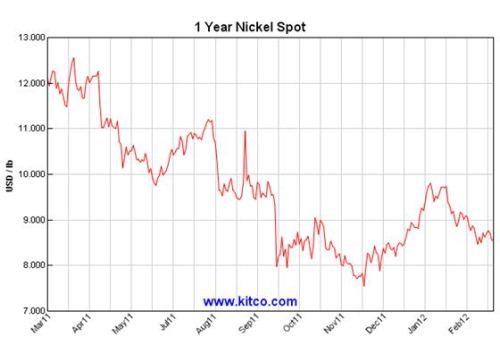

Nickel has dropped by 30 per cent on the London Metal Exchange over the past year, largely as a result of cheap pig nickel.

The situation in Indonesia is that miners with Contracts of Work, including heavyweights Freeport-McMoRan Copper & Gold and Newmont Mining, will be allowed to export ores until 2014.

The immediate ban will mostly affect small miners, as the country’s major nickel producers PT Vale Indonesia and PT Aneka Tambang have already started local processing.

The decree, signed by Energy and Mineral Resources Minister Jero Wacik in February, will ensure miners process ores locally, boosting state revenues and ensuring supplies and investments in the local industry.

Exports will be allowed in processed metal, such as ferronickel and nickel-in-matte, and smelter- or chemical-grade alumina.

It is understood that business license holders could be exempted if they submit ore processing plans.

Indonesia shipped 25.7 million tons of nickel ore to China last year, according to Chinese customs data, which compares with 22.1 million tons from the Philippines, making Indonesia the biggest supplier to China.

Indonesia supplied China with 36.1 million tons of bauxite, while Australia sold 8.4 million tons, ranking as the second-biggest supplier, according to official data.

The critical trade market impact would be that Indonesia exports more refined metal over primary ore.

It produces 15 per cent of global nickel ore and just one per cent of refined nickel.

Chinese nickel- pig iron makers will therefore find it difficult to fully replace lost Indonesian supplies as ore from the Philippines is used more for its iron content.

Furthermore, nickel-bearing ores from Indonesia are generally laterite ores, which means Chinese production of nickel-pig iron will be affected.

Nickel laterite ore can be processed into nickel-pig iron as a substitute for the refined metal for use in stainless steel.

This situation has had a dramatic negative impact on nickel prices over recent years, so hopefully things will improve significantly.

The Chinese to some extent had already begun to purchase more refined nickel, as pig iron has become more expensive over the past six months.

Nickel pig iron has typically been a source of swing production – meaning it’s there when nickel prices are robust, but falls away when prices ease.

In terms of demand-side factors, looser capital rules that have recently been implemented could also have a major impact in terms of raising economic expectations for China, which in turn could drive base-metal prices higher on the expectation of increased demand.

It certainly seems to have played a role in terms of the recent price performance of copper during 2012.

So the outlook is positive in my view for nickel plays for 2012 and beyond.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report