ONE OFF THE WOOD: Predictive Discovery (ASX: PDI) managing director Paul Roberts dropped by to tell us how the company is progressing at its gold prospects in eastern Burkina Faso.

You recently announced drilling and metallurgical results from your Bongou prospect, what light do they shed on the Predictive Discovery story?

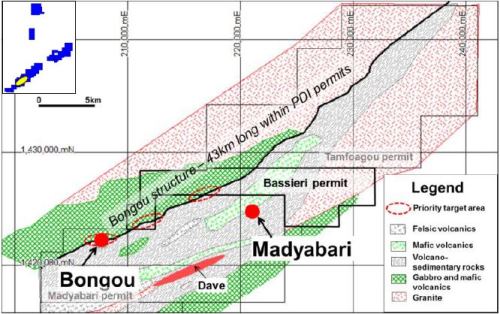

The Predictive Discovery story is about taking a strong technical approach to exploring one very large, 95 to 100 per cent-owned ground position in two adjacent highly prospective greenstone belts which contain abundant artisanal gold workings.

We hold some 1600 square kilometres in Burkina Faso, which has recently emerged as an established gold mining hub.

Our exploration has achieved encouraging drill results from multiple prospects. We are now accumulating those prospects with the intention of turning them into a large mining operation feeding a central mill.

What can you tell us about the recent results?

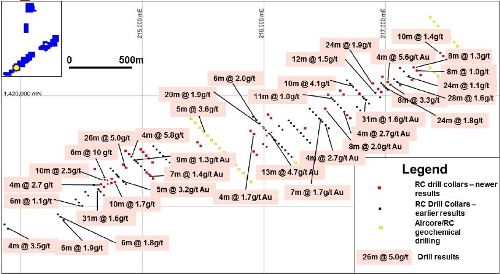

By most standards it was a small program of drilling but it delivered big in terms of results including 48 metres at 4.3g/t gold, including 16m at 9.7g/t gold and 23m at 6.9g/t gold, including 16m at 8.9g/t gold.

These are close to true width intercepts, and importantly, correlate to previous intercepts of 20m at 4.8g/t gold and 10m at 7.4g/t gold.

These seem to appear in a panel of high-grade mineralisation open at depth and potentially plunging to the east.

Geochemical results indicate we may find more Bongou-style mineralisation nearby, expanding potential for discovering substantial, good grade gold mineralisation in a small area.

Is Bongou your main focus?

It’s where we’ve achieved the best combination of continuity, grade and width.

Saying that, we have many prospects we believe have potential to deliver economic resources.

It’s really a matter of knitting them together to create a significant mining operation.

What about your other prospects?

We’ve achieved good results at the Dave prospect, a big system with gold mineralisation over about 5km of strike that remains open, eight kilometres from Bongou – but they’ve been in the moderate-grade category.

We have Dave-style mineralisation from other areas of bedrock geochemical anomalies in the 20km long Laterite Hill Grid in prospects such as Laterite Hill itself and Prospect 71.

We’ve also drilled the Solna and Tambiri prospects up at Bangaba some 60km to the north and acquired the Bira ground, a similar distance to the north east that shows consistent 20m widths over at least 500m of strike with good mineralisation continuity and grades of 1 to 2g/t gold.

What results have you been able to achieve at Bongou?

We recommenced our activities this field season determined to focus on grade.

We focused our first round of drilling on prospects most likely to deliver the most favourable combination of continuity, grade, and width.

We obtained good results from several prospects, but realised Bongou fitted those criteria the best, so we focused most of our work there.

Our March drilling produced the best drill results we’ve seen so far, displaying a consistent pattern of high-grade gold mineralisation on the contact between granite and gabbro at Bongou, which is open to depth.

The known Bongou gold mineralisation is limited to around 150m of strike, leading us to step our exploration outwards to try and find more Bongou-style anomalies in the surrounding areas.

Geochemical drilling suggests we’re getting those anomalies 500m or more from Bongou, but we’ve still a long way to go to test the whole area.

What has the Bongou drilling told you?

We have a zone of high-grade mineralisation, which is averaging about 10m in true thickness, which, at a 3g/t cut-off, contains an average grade so far of around 10g/t.

We have, what you could describe as, a nice slab of high-grade mineralisation anyone would be able to mine profitably; as long as follow-up drilling proves it continues with consistency to depth.

We then have lower-grades of gold along the high-grade’s southern margin, so the true width of the gold mineralised part of the system averages, maybe, 25m but ranges up to nearly 50m, which should offer good stripping ratios for open pit mining.

Geological mapping along the fault zone at Bongou identified outcrops of granite, what is the significance of this?

The Bongou mineralisation is new for this area as it’s hosted in a granite body surrounded by mafic rocks.

There is a series of small granite outcrops surrounded by a wide plain of soil and alluvial cover along strike to the east and west, which is important as a number of granite-hosted Bongou-like ore deposits could be sitting under thin cover nearby.

These granite outcrops lie close to a large, deep 43km long fault within our permits, which we are certain is the fault that has delivered the fluids to form the Bongou gold mineralisation.

We want to determine where that combination of granite and the major fault may reappear, especially when the granite is in contact with mafic rocks like at Bongou.

In the immediate vicinity of the drilled area, we’ve identified several areas of interest within about 2km of strike.

Adding to this, we have identified other targets on the major fault through mapping and geophysics 4km and 10km to the northeast.

What did your recent exploration work at Bongou include?

An electrical geophysical survey, covering about 2.5km of strike, as well as bedrock geochemical drilling of the electrical geophysical anomalies.

This geochemical drilling turned up more Bongou-scale anomalies, one of which is definitely in altered granite. We are now trenching that granite to see how it looks.

We also carried out metallurgical testwork, not only at Bongou, but also on other prospects, including the Dave prospect nearby and the higher grade Tambiri and Solna prospects to the north.

What did that metallurgical testwork return?

It gave us high-gold recoveries from all of the prospects we tested.

The Bongou prospect returned recoveries of 94 per cent gold while the Solna and Tambiri tests recovered 96 per cent and 92 per cent gold respectively.

At Dave, we focused on the possibility of heap leach gold recovery from moderate grade oxide mineralisation.

At Dave there’s an average depth of oxidation of about 50m where there could be quite a lot of material that could be put on a heap.

The testwork indicated heap leach is possible. Bottle roll cyanide leaching of reverse circulation drill chips and powder gave us 89 per cent recovery.

An economical heap leach operation should be recovering more than 60 per cent of the gold. While there is a long way to go yet, with agglomeration, we think this may be achievable at Dave.

You did the metallurgy early, were you pleased with those results?

Absolutely; it reduced a big risk element in some of our key prospects.

We’ve seen no evidence of refractory gold, which can be cause for concern in some West African gold deposits.

We can also see the possibility of recovering gold economically from some of the lower grade material as a supplement to standard CIL treatment of higher grade material from such places as Bongou and Tambiri.

If we can find more mineralisation with the same characteristics as Bongou, it gives us the opportunity to rapidly drill out resources with above average grades, which can get us started with high profitability and rapid capital payback earlier.

In the current, very difficult, investment climate, my picture of the near future is that we should aim to build on the Bongou results to identify enough reserves to get started with high-grade ore production, possibly not with a huge mill throughput to begin with.

This could keep initial capital costs relatively low and provide a springboard for increasing gold production as time goes on.

Producing and being profitable allows you to move onto the lower grade material?

That’s right and a heap leach operation on a prospect like Dave would be a classic case in point.

Getting started and producing gold would also allow time to progressively develop other prospects in our large ground holding.

We’ve always said we’re aiming to get more than two million ounces at over 2g/t here and we believe we have the ground position to deliver that.