CONFERENCE CALLER: With the Paydirt Africa Down Under Conference kicking off next week, we thought we would take a look at what a few of the exhibiting companies have been up to lately.

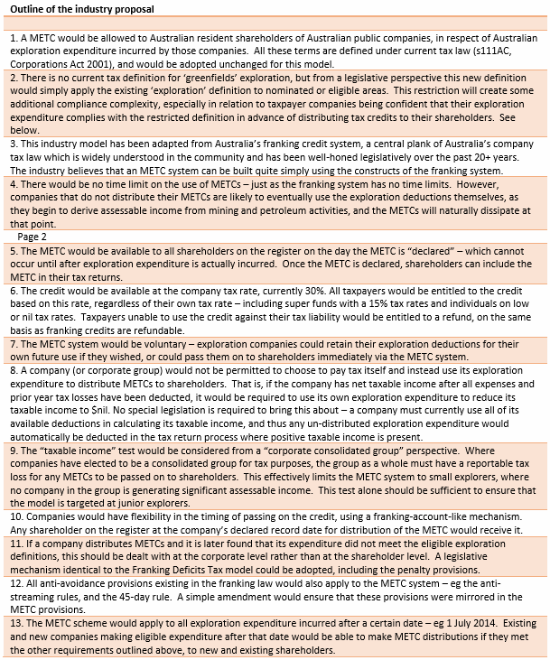

Gryphon Minerals (ASX: GRY)

Permitting for the Mining Licence at Gryphon’s Banfora gold project in Burkina Faso, West Africa is apparently progressing well with the company anticipating it completion by the fourth quarter 2013.

As part of this process Gryphon recently presented its development plans to the National Bureau of Environmental Assessments technical committee in Burkina Faso.

Heap Leach Studies at Banfora have returned gold recoveries of up to 85 per cent at the Nogbele deposit.

Gryphon said this test work confirms the amenability of the low grade halo material at the Nogbele deposit to heap leach processing. Heap leach scoping studies are currently underway.

Reserve drilling has confirmed further high-grade gold mineralisation at Nogbele, while reconfirming the current geological model as well as demonstrating continuity of higher grade zones at the northern part of the Nogbele deposit.

Drill results include:

4 metres at 34.34g/t gold from 30 metres;

4m at 33.04g/t gold from 26m; and

4m at 32.73g/t gold from 14m.

Gryphon has ongoing detailed environmental and social baseline surveys continuing for mine permitting.

It is also conducting project optimisation studies following on from the January BFS to appraise reductions to capital and production costs.

The company boasted a cash balance of $52 million at the end of June quarter 2013.

Golden Rim Resources (ASX: GMR)

Golden Rim Resources has commenced an Environmental Impact Assessment (EIA) as part of a Bankable Feasibility Study (BFS) on the company’s Balogo project in Burkina Faso.

SOCREGE Sarl is conducting the EIA which is expected to be completed by the end of

June 2015.

Other components of the BFS are expected to commence in late September 2014, after the rainy season.

Initially Golden Rim intends to complete an infill drilling program at Netiana to upgrade the gold resource.

It plans to use some of these drill holes for geotechnical, metallurgical and hydrological purposes. The drilling will be followed by mining and engineering studies.

The BFS will assess the economic viability of installing a modular 30 tonnes per hour gravity and CIL plant to exploit the resource at Netiana.

Golden Rim has outlined a high-grade Inferred Resource at the Netiana Lodes at

Balogo of 850,000 tonnes at 6.8g/t gold for 185,000 ounces of gold.

Golden Rim has also completed a scoping study on the Netiana Lodes which indicates the resource can support a robust, high margin, low capital cost, open pit mine development.

IMX Resources (ASX: IXR)

IMX Resources recently announced an updated global Mineral Resource estimate for the company’s Ntaka Hill nickel sulphide project that comprised the updated Sleeping Giant deposit Mineral Resource estimate, the Zeppelin Mineral Resource estimate, and the existing Mineral Resource estimates for J Zone, G Zone and M Zone as of March 2012.

Recently completed resource modelling work indicated the Sleeping Giant deposit now comprises the Mineral Resources of H Zone, L Zone, NAD-013 zone and Sleeping Giant, which now form a larger single deposit within the Ntaka Hill mineralised system.

The compilation of data that comprises the Sleeping Giant deposit Mineral Resource estimate, the Zeppelin Mineral Resource estimate and the existing Mineral Resource estimates for J Zone, G Zone and M Zone confirms an increase in contained nickel at a substantially increased grade for the Inferred Resource category.

The total Measured and Indicated Mineral Resources at Ntaka Hill are currently 20.3 million tonnes at 0.58 per cent nickel (and 0.13 per cent copper) for 117,880 tonnes of contained nickel, and the total Inferred Mineral Resources at Ntaka Hill are currently 35.9 million tonnes at 0.66 per cent nickel (and 0.14 per cent copper) for 238,500 tonnes of contained nickel.

Tiger Resources (ASX: TGS)

Tiger Resources recently announced an upgrade to the Indicated and Inferred Resources at the Sase Central deposit, part of the company’s 100 per cent-owned Lupoto copper project in the Democratic Republic of Congo.

The resource estimate was independently completed by Cube Consulting and updated the maiden estimate Tiger completed in March 2011 following additional diamond drilling (DD) and reverse circulation (RC) drilling completed since then.

The Indicated Resource for the Sase Central deposit came in at 9.6 million tonnes at 1.39 per cent copper containing 134,000 tonnes of copper (and 5,000 tonnes of cobalt).

The change to the Indicated Resource represented an increase of 173 per cent (from 49,000 tonnes copper in March 2011).

The deposit has an Inferred Resource of 2.8 million tonnes at 1.21 per cent copper containing 34,000 tonnes of copper (and 1,000 tonnes of cobalt).

The Sase deposit now has a combined Indicated and Inferred Resource of 168,000 tonnes of copper.

The updated mineral resource estimate was based on 51 diamond drilling holes totalling 7,779m and 50 RC holes totalling 4,901m.

In addition, 448 air core (AC) holes totalling 16,743m were completed but these holes were not used for the estimation.

Tiger Resources did, however, say they do, however, provide a guide to the interpretation of the copper mineralisation domain.

.jpg)

.jpg)

.jpg)