Mention Nevada and most people think of Las Vegas, but a package of three highly-prospective tenements acquired by this junior gold explorer has stacked all the odds in its favour.

Cassini Resources (ASX:CZI) successfully listed on the Australian Securities Exchange in January 2011 during a period that saw many other IPOs fail to achieve the same feat.

Cassini garnered support for its listing on the back of a tenement package of four early-stage projects in Western Australia located in the West Musgrave, out near Warburton; Forrestania; Peak Charles; and the Eucla Basin.

“We listed on the back of some tenements we believed, and still do believe, to be really good assets,” Cassini Resources managing director Richard Bevan told The Inside Story.

“They are all early-stage projects, but we believe they have a great deal of potential.”

The potential of Cassini’s WA projects is exemplified by the Musgrave project, which is situated in what had been a poorly explored province until the discovery of BHP Billiton’s Nebo and Babel nickel-copper-Platinum Group Element (PGE) sulphide deposits initiated a surge of aggressive exploration activity.

A number of gravity and magnetic anomalies have been identified on the Cassini leases which appear to have similar characteristics to the nearby Nebo – Babel deposits, none of which have been subjected to any serious drilling.

Cassini is expecting to finalise an access agreement with traditional owners at Musgrave by the end of May, which should result in the granting of exploration licences at the project.

“Once that is done we have a ground geochemistry program we anticipate commencing around July / August,” Bevan said.

“We are looking to add value and progress all of our WA projects, but our priority is progressing our North American projects.”

Casssini’s North America projects are set to become the envy of the ASX junior gold exploration sector.

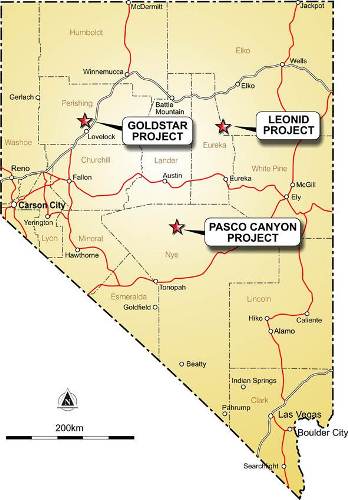

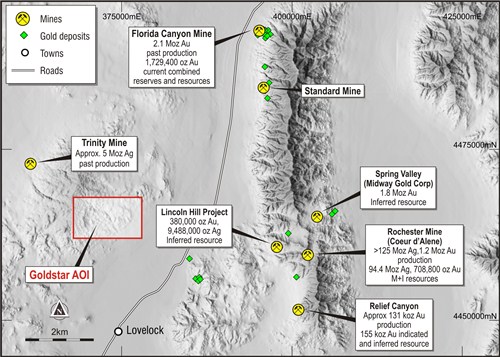

Cassini Resources Nevada projects map.

“We have acquired three highly-prospective projects in Nevada that are situated amongst a number of multi-million ounce gold deposits and operating mines,” Bevan said.

“These projects are a lot more advanced than our Australian projects and provide us with three great opportunities to find something of significance that could possibly become a company maker”

The company is poised to acquire 100 per cent of private Australian company Search Resources, whose United States subsidiary company has signed a Joint Venture agreement with Nevada‐based gold/silver-focused exploration company Renaissance Gold.

Cassini will acquire the rights of the existing JV agreements to earn a 70 per cent equity interest in three prospective gold exploration projects in Nevada.

The most advanced of these projects is Pasco Canyon, which is endowed with existing defined drill targets.

The company has re-interpreted the geology at Pasco Canyon and will drill two to four deeper holes against the direction of previous drilling to intercept the mineralised zone.

“The three projects are all at slightly different stages of advancement,” Bevan explained.

“The Pasco Canyon project is ready to drill and we have already had the drilling permits granted.

“We are just finalising the commencement date for that drilling program and hopefully will be drilling by July/ August.”

The company’s second project in Nevada is Goldstar where rock chip sampling returned impressive results including 19.8 grams per tonne gold and 1,213 grams per tonne silver from quartz veining at surface, but is yet to be drilled.

“There is more sampling and mapping work to be done at Goldstar but we anticipate drilling on that project by the end of the year,” Bevan said.

The final project is the Leonid project, which is at an earlier stage of advancement than Pasco Canyon or Goldstar, however the company feels it could hold the most potential.

Over seven kilometres of anomalous gold mineralisation is already identified at Leonid.

Cassini intends following up exploration work by Renaissance Gold that has defined drill targets.

Leonid is situated within the Carlin Trend, which is considered to be one of the world’s richest gold mining districts.

The Carlin Trend is host to seven 20Moz-plus gold deposits, including the largest gold assets of major mining companies Newmont and Barrick Gold.

By 2010 mines operating in the Carlin Trend had produced over 100Moz of gold.

“The Carlin Trend hosts a number of significant deposits, which are located in close proximity, some just 20 kilometres away, from Leonid,” Bevan said.

“The early signs emerging from Leonid are that all the markers and pathfinders for a deposit are there.

“We expect to be in a position where we can commence drilling Leonid by the end of the year but we still have some preliminary work in terms of soil geochemistry testing as well as some surveying and mapping activity.

“In the next six months, before winter sets in over there, we should be able to progress all of these projects.”

Cassini is confident the bulk of the work required to progress its American-based project portfolio is not in the high-cost bracket.

The drilling to be conducted at Pasco is probably its most expensive task but the other groundwork is reasonably low-cost, which means the company will be able to keep proving up the project models without a huge financial outlay.

To understand how prospective these projects are, Bevan said it was important the market began to understand how prolific the state of Nevada is in terms of gold production.

In 2011 Nevada produced some 6.1 million ounces of gold, making it responsible for approximately 83 per cent of US gold production that year.

The US sits third in on the list of gold producing countries. If you were to take the US out of the list and replace it with Nevada it would come in at number six.

Despite having been explored and mined for over 150 years the region continues to yield new discoveries.

Cassini’s Nevada projects are situated near a number of multi-million ounce gold deposits

“Nevada is a mining state providing a well-trodden path for explorers with excellent infrastructure and expertise and equipment, all readily available,” Bevan said.

“There is a lot of exploration activity happening that significantly de-risks our projects and we also have a 30 per cent Joint Venture partner that resides in Nevada.

“We are also fortunate having our newly appointed executive director – exploration David Johnson, based in Salt Lake City, Utah.

“That combination provides us with a strong technical background with strong local links enabling them to access services and expertise.”

Johnson is an Australian-trained geoscientist who has worked for such companies such as Western Mining, Rio Tinto, LionOre and Independence Group.

His appointment reflects the make-up of the Cassini Board with the company’s chairman, Mike Young being a Toronto-trained geologist now based in Perth.

Young is also managing director of BC Iron, which successfully made the transition from iron ore exploration company to become the most recent iron ore producer in WA’s Pilbara region.

As exciting as the company’s Nevada projects are Bevan indicated Cassini Resources has no intention of turning its back on the WA projects it listed on.

“Our intention is to operate the two in tandem,” Bevan said.

“We have the capital to run both but we need to be mindful how we spend our money.

“The good thing with the Nevada assets, especially with some of the early drilling programs, is we should know sooner rather than later if we do have something there.

“We can then sit back and assess where we would be best placed to allocate our capital in terms of adding value.”

Cassini Resources Limited (ASX:CZI)

…The Short Story

HEAD OFFICE

945 Wellington Street

West Perth WA 6005

Phone: +61 8 9322 7600

Fax: + 61 8 9322 7602

Email: admin@cassiniresources.com.au

Web: www.cassiniresources.com.au

DIRECTORS and MANAGEMENT

Mike Young, Richard Bevan, Phil Warren, Greg Miles

MAJOR SHAREHOLDERS

Richard Bevan 7.44%

Freelight Nominees 6.80%

Mike Young 6.47%

SHARES ON ISSUE

18.75 million

MARKET CAPITALISATION

$2.81 million (at 15/05/12)

.JPG)

.jpg)