Saturn Metals Priming Apollo Hill for Lift-off

THE INSIDE STORY: Saturn Metals (ASX: STN) listed on the ASX with the purpose of giving the Apollo Hill gold project the attention its deserves and has not received.

Saturn Metals became the beneficiary of the exploration success enjoyed by Peel Mining (ASX: PEX) at its base metals projects in the Cobar Basin of New South Wales.

Peel originally acquired the Apollo Hill gold assets hoping to become a West Australian gold producer; however, its discovery of the Mallee Bull copper deposit shifted its gaze.

Peel always considered the value of Apollo Hill, but also realised that a gold project with such potential sitting idle was wasteful.

There are few newly-listed, gold exploration plays with a healthier diagnosis than Saturn Metals.

Not even six months into its ASX-existence, Saturn has a gold project totalling around 1,076 square kilometres of contiguous tenements in 23 mining, exploration and prospecting licenses, located in the heart of one of Australia’s highest producing regions.

The company raised $7 million in its IPO and at March this year it still had a healthy figure of around $6.5 million in the company coffers.

It has also been successful in applying for a grant under a recent round of the Western Australian Government’s Exploration Incentive Scheme (EIS) that will cover 50 per cent of the cost of two RC/diamond holes planned to follow up on historic and recent drilling at the project.

“Our strategic land position is right in the heart of the Eastern Goldfields of Western Australia,” Saturn Metals managing director Ian Bamborough told The Resources Roadhouse.

“If you even thought, on a very basic level, about the synchronicity of plus-one million-ounce major deposits, it becomes obvious that there is a large gap in the strongest greenstone belt of the region and it sits pretty much where we are.”

The Apollo Hill project is approximately 60 kilometres southeast of the gold mining and processing town of Leonora in a neighbourhood dotted by numerous companies currently mining multi-million-ounce gold deposits.

The project came with an established JORC code 2012-compliant Inferred Resource of 17.2 million tonnes at 0.9 grams per tonne gold for 505,000 ounces of gold using a 0.5 g/t cut-off (maximum depth of the resource at 180m below surface).

The Apollo Hill project comprises two deposits, the main Apollo Hill deposit in the north of the project area, and the smaller Ra deposit in the south.

At Apollo Hill, Peel Mining had identified two zones of mineralisation: The West (or Main) Zone and the East Zone and when it handed the project over the Resource extended for about 1,100m in strike.

Peel had tested the Apollo Hill mineralisation using 30m spaced, 45 degrees trending traverses of drill holes.

For most traverses, the upper approximately 50m was tested by holes spaced at around 20 to 30m.

Below this depth the coverage is variable, ranging from around 20m spacing on some sections to commonly greater than 60m.

The western mineralised domain has an average width of about 70m while the eastern domain has an average width of about 100m.

Metallurgical testwork by Peel demonstrated gold extraction levels of more than 60 per cent by gravity separation alone and greater than 92 per cent of gold extractable via gravity and cyanidation.

Saturn Metals was quick to declare its intentions for growing the Resources and to extend the known mineralisation.

An airborne magnetic and radiometric survey was completed in March, providing district scale gold targeting information.

This was followed by a high-resolution ground gravity survey over two highly prospective areas within the tenement package.

The company expects the results from both surveys will improve its exploration targeting ability at the regional scale.

Since listing, Saturn has completed around 4,300m of RC drilling and a 1200m program of diamond drilling and has returned the RC rig to carry out further drilling.

Saturn anticipates the drilling will achieve on a multi-pronged basis, the first being to extend and open the system, while the next is about upgrading the current Resource, which it expects to have finished by around September.

The company is confident of developing Apollo into being a two-million-ounce gold district.

“We have conducted some specific drilling targeting higher-grade plunging shoots within the Apollo Hill gold system and that is going to do a couple of things,” Bamborough explained.

“If we find a high-grade shoot within the greater system then there is potential to lift the grade of the system.

“To put that in context: a 0.1 grams per tonne uplift on a 17 million tonne Resource will provide a further 50,000 ounces.

“We want to get above that 0.9 grams per tonne hurdle and bring that grade up over the one gram per tonne mark, which will mostly likely place us in an improved position when compared to our peers.

“The higher-grade shoots – if they emerge into what we believe they could be – could develop into being ore bodies within their own right within the bigger low-grade halo.

“There is tremendous leverage for making this project better.”

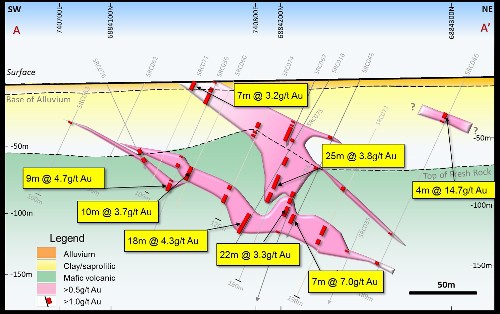

Recent near-surface extensional assay results from the earlier RC drilling compared favourably with historic drill intersections from Apollo Hill.

Better results included:

AHRC0024

12 metres at 2.8 grams per tonne gold from 4m, including 3m at 8.8g/t gold from 13m;

AHRC0019

20m at 2.5g/t gold from 52m and 11m at 2.28g/t gold from 84m within, 100m at 1.01g/t Au from 7m;

AHRC0029

22m at 1.01g/t gold from 52m, including 11m at 1.49g/t gold from 52m;

AHRC0032

10m at 1.5g/t gold from 49m;

AHRC0034

6m at 2.41g/t gold from 53m; and

AHRC0028

34m at 0.45g/t gold from 76m;

Saturn moved seamlessly into its maiden diamond drilling program at Apollo Hill comprising approximately 1,200m in nine holes to follow up on the Saturn RC drilling that had further highlighted the potential for several stacked, higher grade plunging shoots.

In addition to Saturn’s new RC results, intersections from historic drilling included 2m at 69.6g/t gold from 146m and 5.3m at 10.3g/t gold from 70.7m.

“The diamond drilling that we have just finished has been very much about finding further evidence of the higher-grade architecture and about having a really good look at the entire thing as well,” Bamborough said.

“Because of the way this area has been historically approached, generally as a big low-grade deposit drilled with wide spaced holes, I think people have had the mindset that this is all it can be.

“I’ve taken that hat off and have decided to look within at these beautiful gold shoots that are sparsely drilled.

“The higher grade historic intersections and our new drilling results are telling us how and where to focus.

“If these results had been achieved at a project such as Jundee, owners of the Newmont and Northern Star ilk would have been right in there with underground drill rigs giving It a good hammering.

“My vision is to create a paradigm shift for people on the deposit.

“Yes, we can make it bigger, but this is how we are now going to make it better.

“What I can say now, is that the geology that we have seen from the diamond holes is adding weight to those theories.”

Saturn Metals Limited (ASX: STN)

… The Short Story

HEAD OFFICE

Unit 1

34 Kings Park Road

West Perth WA 6005

Ph: (08) 6424 8695

Email: info@saturnmetals.com.au

Web: www.saturnmetals.com.au

DIRECTORS

Ian Bamborough, Rob Tyson, Andrew Venn