Old Campaigners on Standby for EV Revolution

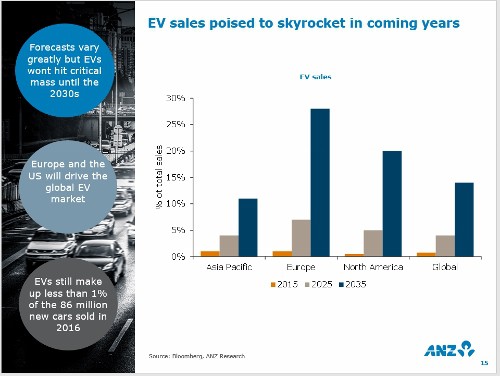

COMMODITY CAPERS: Some analysts suggest that EV sales will be responsible for around 25 per cent, and more, of total vehicle sales by the end of 2035 from the current levels of around one per cent.

Coming off a relatively low base the projected growth could have a significant effect on markets for certain commodities.

Nickel and copper are two traditional commodities that have found the running comfortable with the upsurge in interest for battery metals.

Although lithium and cobalt have been sneaking away with the bulk of the headlines, nickel and copper are also integral parts of the lithium-ion battery make-up, and as such are enjoying some new-found fame.

In his presentation to the 2018 RIU Explorers Conference, ANZ senior commodity strategist Daniel Hynes said investors have woken up to the impact lithium-ion batteries have had on these two markets.

“Environmental issues have evolved from being secondary policy targets to one of the top priorities for many countries over the past few years,” Hynes said.

“Certainly, China has been quite important in driving this dynamic over the past few years and clearly all the headlines have been focused on sectors such as the Electric Vehicle market and what that can do for commodity demand.

“No-one really knows the level of adoption that the market place will take.

“That certainly has been a big reason behind the rebound of nickel prices, even though the volumes are going to be relatively low.

“It is interesting to note the differences in the amounts of copper used in a conventional car as opposed to a battery EV.

“Essentially nine times the amount of copper is used.

“The dynamics are quite strong, and we do expect to see the markets turning.”

Currently, the EV/ lithium-ion battery chatter is creating a strong global market interest for nickel, which is receiving support, albeit in the short-term by higher stainless-steel production.

Australian mine production is expected to fall to 176,000 tonnes in 2017–18 before recovering slightly to 183,000 tonnes in 2018–19 while the country’s nickel export earnings are expected to fall slightly to $2.1 billion in 2017–18, before rebounding to $2.3 billion in 2018–19.

In a metals&ROCK research note released in April, Morgan Stanley noted that the main driver to global nickel demand to be, “any change in the level of activity in China’s stainless steel industry”.

Seventy per cent of the world’s primary nickel supply is gobbled up by Chinese smelters as they produce 54 per cent of the world’s total 46 million tonnes of stainless steel.

“And so far in 2017, China’s SS-output rate’s up (+23 per cent year-on-year, Jan-Feb),” Morgan Stanley reported.

“Roughly in line with the general lift in output of its +820 million tonnes per annum carbon-steel industry – buoyed by Q1’s credit surge, and a central government sponsored infrastructure program.”

The Department of Industry, Innovation and Science noted a recent rise in nickel prices attributing markets factoring in growing demand linked to lithium-ion batteries, however it also said that it was not clear that the immediate boost to prices will persist.

“Although sales of electric vehicles are rising sharply, at this stage, batteries still account for a small share of nickel sales, and stainless steel is still estimated to account for around two-thirds of nickel consumption over the outlook period,” the department said in its December Quarter Resources and Energy Quarterly.

Although copper does have a part to play in the EV revolution, currently it is its older stomping grounds that are contributing to its recent positive run.

Source: DIIS

DIIS cited the London Metal Exchange (LME) copper price estimate to have averaged US$6,810 a tonne in the December quarter, the highest level since September quarter 2014.

Credit for this rise was given to growth in global industrial production and several supply disruptions, including incidents at KGHM’s Glogow smelter in Poland and Rio Tinto’s Garfield operations in the US.

Although copper inventories on the major global exchanges fell by 6.4 per cent quarter on quarter, contributing to higher prices in the December quarter these are expected to wane in 2018 with the LME copper price forecast to average US$6,340 a tonne as supplies increase.

A pick up in consumption over supply has forecasters predicting a rise in copper prices to US$6,490 a tonne in 2019.

“Global copper consumption is forecast to rise from 24 million tonnes in 2017 to 25 million tonnes in 2019, representing an average increase of 3.2 per cent each year,” DIIS said.

“Higher copper consumption will be supported by firm growth in global industrial production and higher investment in energy infrastructure.

“Emerging economies are expected to drive much of the growth in copper consumption over the next two years.”

China is expected to lead this copper consumptive period.

The country already accounts for around 50 per cent of global demand and looks to increase that number as it makes improvements to the nation’s power grid and enjoys further growth in the construction and manufacturing sectors.

The coming shortfall will kick in once global demand for electric cars and renewable energy takes off, leading to stronger growth in copper consumption over the next two years.

“Increased global production of electric vehicles…is expected to raise copper consumption by around 300,000 tonnes annually in 2018 and 2019,” DIIS said.

“Copper is used extensively in renewable energy technology and infrastructure, spending on which is expected to increase strongly over the outlook period.

“Global electricity capacity from renewable sources is expected to increase by 4.4 per cent annually over the outlook period.”