As I’ve been at pains to point out, despite all of the doom and gloom pervading the resource sector at present, one thing for sure is that there are a host of supply-side factors that will ensure that commodity price remain robust over the medium to longer-term.

Gone are the days of steadily declining commodity prices as a result of new, lower-cost developments and efficiencies through new technologies.

The big issue in mining these days is the fact that pretty much all of the low-hanging fruit (in the form of easily accessible, large-scale, high-grade deposits) have already been identified and mined.

To get their hands on world-class projects, the world’s heavyweight miners these days have to head for less-friendly parts of the world where political situations are uncertain and infrastructure challenges are immense.

Even formerly ‘mining-friendly’ destinations like Australia and Canada have become less so – meaning miners have to factor in a whole new range of risk factors when assessing new project developments.

At the end of the day this means mining companies will justifiably seek higher prices for their products before committing to higher risk, higher cost developments.

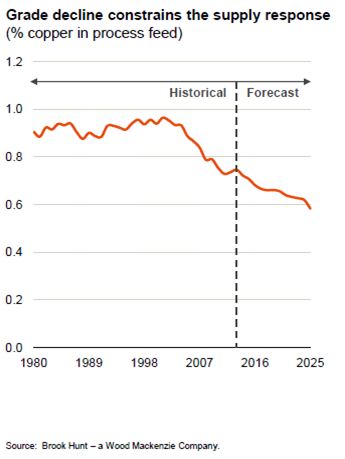

If we turn our attention to copper, head grades are declining alarmingly at virtually all of the world’s major copper mines, forcing up production costs and negatively affecting output.

The average head grade at the world’s major mines has fallen by around 20 per cent over the past decade, meaning miners have to dig 20 per cent more earth just to maintain production levels of a decade ago. And the grade decline is set to continue.

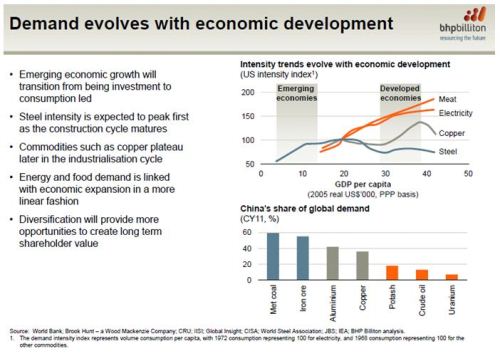

The second slide from BHP’s recent copper presentation highlights the change in economic growth as economies mature.

It’s already happened in most Western economies like the USA and Europe, where by growth evolves from being predominantly investment-related to more consumption-generated.

From the charts above, the intensity of copper use increases when economies like China’s begin to evolve from being heavily investment-driven (as they are now) to being more consumption-driven.

This occurs as citizens in emerging economies seek the sorts of lifestyle objects (motor vehicles, household white-goods, electronic items, etc.) that we take for granted.

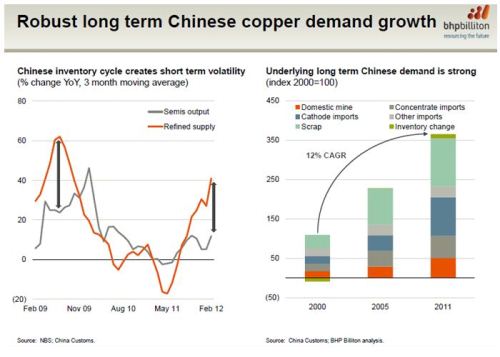

Irrespective of near-term fluctuations due to market sentiment, copper consumption is set to continue rising strongly in emerging economies like China, Brazil and India.

For the first five months of 2012, copper imports by China increased by 52 per cent year-on-year, as demand for the red metal continued to soar.

Chinese demand is likely to pick up during the coming months as authorities seek to stabilise the economy with new infrastructure measures.

New home appliance and car purchase subsidies currently under consideration in the country should help support copper demand.

Chinese buying helped copper prices surge some 140 per cent last year.

Prices are bound to move into positive territory, though most of the copper that China imported in May went for inventory build-up.

In 2011, China accounted for nearly 40 per cent of the 19.74 million tonnes of refined copper used worldwide.

Brazil too has emerged as a growing user of copper.

From 2002 to 2008, per capita copper consumption in Brazil increased 50 per cent to 2.1 kilograms, approximately 30 per cent higher than the country’s GDP growth in those years.

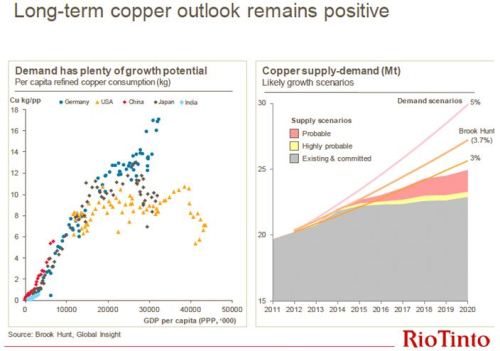

The graphic from Rio Tinto’s recent base metals presentation tells a similar story to that of BHP. Intensity of usage is rising rapidly amongst the world’s emerging economies.

Interestingly too, the head of Xstrata’s copper unit Charlie Sartain commented recently that despite the European situation, the fundamentals remain the same for copper.

“There’s still strong demand for copper in China and we’re seeing a slight recovery in the US economy,” he said.

It also has supply challenges of its own, with its copper output likely to dip slightly during the first half of the year as the world’s No 3 copper mine, Collahuasi, in which it has a stake, battles declining ore grades.

The annual CESCO week copper conference recently put No.1 producer Chile’s woes firmly back in the spotlight.

The truth is that there are no easy fixes for tumbling ore grades at massive mines in northern Chile, along with protests over key energy projects that are threatening mining expansions.

While Chile continues to produce a third of the world’s copper supply and holds an estimated 28 per cent of global reserves, the nation needs to fight on multiple fronts to boost annual output to the over 7 million tonnes it aspires to produce by the end of the decade.

“We’re frankly at a very delicate moment, especially in terms of energy,” Joaquin Villarino, head of the country’s Mining Council that represents Chile’s biggest miners, said at the forum on energy.

“If we’re not able to solve several problems, mining isn’t going to develop in the country or it will develop less than we would like.”

With no significant deposits slated to come on-line this year, so-called “strike season” yet to kick off in Chile and both Xstrata and Rio predicting ebbs in their production during the first half of 2012, Chilean miners are predicting tight supply will offset any Chinese slowdown.

Codelco has an ambitious plan to boost its annual output to 2.1 million tonnes by 2020, but forecasts a slight ebb in production this year.

Chile is seen attracting $1 billion in mining investment through 2020, but some analysts have questioned that figure as overly upbeat.

Last year Antofagasta Minerals launched its flagship mine Esperanza, one of the few promising deposits to come online in a copper market defined by its scarcity of new projects.

But Esperanza has disappointed, contributing to Antofagasta missing its 2011 copper output target and factoring into their veteran CEO Marcelo Awad’s abrupt resignation earlier this year.

Few deposits are more emblematic of Chile’s potential decline than its massive but tired, water-short and energy-strapped copper mines in the mineral-rich Atacama Desert.

Codelco’s century-old, behemoth Chuquicamata mine has seen its output drop from 528,000 tonnes in 2010 to 443,000 tonnes last year, chiefly on grade woes.

At the end of the day, it’s important to try and remain calm and ignore the frenzied headlines of negativity that one is currently exposed to on a daily basis.

Remember that the world is on an inexorable growth path, led by China and a host of other emerging economies, as the world’s population surges past 7 billion.

Commodity demand will remain robust for decades to come.

Both BHP Billiton and Rio Tinto remain confident about the long-term outlook for copper despite the current market pessimism.

The near-term issues that are impacting miners on a day-to-day basis are actually providing a solid platform for even higher commodity prices in the future.

So continue to retain your perspective, even when everyone else is losing theirs.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report