There has been much speculation and breath holding in anticipation of what may be the next project or destination for Pilbara iron ore producer BC Iron (ASX:BCI).

In 2006, led by its indefatigable managing director Mike Young, BC Iron took an iron ore exploration play located in what was in at the time, inaccessible territory, to emerge as one of the success stories of the junior iron ore sector rush.

Access to infrastructure was the secret behind that success with the company’s Nullagine mine located close to a train station on the Fortescue Metals Group (ASX:FMG) express train to Port Hedland.

BC Iron’s 50:50 Nullagine Joint Venture with FMG now produces iron ore at a rate of five million tonnes per annum.

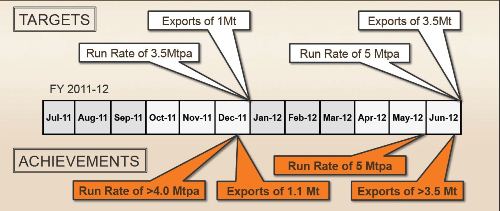

Throughout the 2012 financial year the Joint Venture mined and crushed 3.54 million tonnes of iron ore, resulting in shipment of 3.55 million tonnes.

Ore Reserves at Nullagine have been increased to 41 million tonnes at 57.1 per cent iron and the company is sitting comfortably on a bank balance of over $93 million.

The Nullagine Jint Venture has hit all advancement targets ahead of schedule

History is repeating with infrastructure a factor behind BC Iron recently joining forces with ASX-listed Cleveland Mining (ASX:CDG) to look for projects in the South American country of Brazil.

“It’s a very strategic move in that it covers all of Brazil for Joint Ventures in iron ore,” Young told The Inside Story.

“The Board of Cleveland mining, collectively, has a great deal of in-country experience.

“They have connections with the main players within the country’s infrastructure sector, which is very important.

“Brazil is not much different to Australia in the fact there is lots of iron ore, but there is not a lot of infrastructure.

“Brazil has a domestic pig iron industry if you want to start up small and get a bit of cash flow going.

“With a project of the Nullagine JV you could make money selling into the domestic market – you just wouldn’t make the margins that we are making.”

The Board members of Cleveland Mining are no strangers to BC Iron with FMG non-executive director Russell Scrimshaw and FMG founding member Jim Williams both having a seat at the table.

Russell Scrimshaw was a key person in the relationship between Fortescue and BC Iron.

Cleveland managing director David Mendelawitz is also a FMG alumnus, where he held the position of Head of Business Improvement, while company chairman Don Baily was a founding shareholder and chairman of LionOre Mining before it was purchased by Norilsk Nickel.

Bailey has also been deputy mining director of Rio Tinto running its operations in South America, Southern Africa and Continental Europe.

“That meant that the due diligence required in terms of Cleveland’s Board and management was relatively straight forward,” Young said.

“I think people may now look again at Cleveland and realise it has a really good team.”

Cleveland Mining’s main focus, at present is the Premier gold mine in the company’s Crixás Hub, located in Goiás state in Brazil.

Construction of the Premier mine is nearing completion and Cleveland plans to commence commissioning of the plant shortly.

“They started the gold mine to generate some cash flow as they wanted to be self-funding, which is great as that keeps their capital structure nice and tight, like ours,” Young said.

“That mine serves two purposes: one, it produces gold, which is as good as cash in terms of maintaining liquidity; and it establishes them as miners in Brazil and gives them bona fides with the regulatory bodies.”

Young explained that by establishing a mine in Brazil a company also establishes its bona fides as a miner.

The logic is similar to that pertaining to companies operating in Australia; if a company can demonstrate it can meet the strict approvals processes once it means it can approach the approval of its next project with confidence.

“I have no doubt that if we had looked at another project in Western Australia we would have a gold star next to our name in terms of meeting approval requirements,” Young said.

“And I believe that it’s the same for Cleveland in Brazil.”

As exciting as the new deal is Young said it didn’t mean BC Iron would be shifting its focus from its Pilbara operations or blinker its sights in regards to other acquisitions within WA.

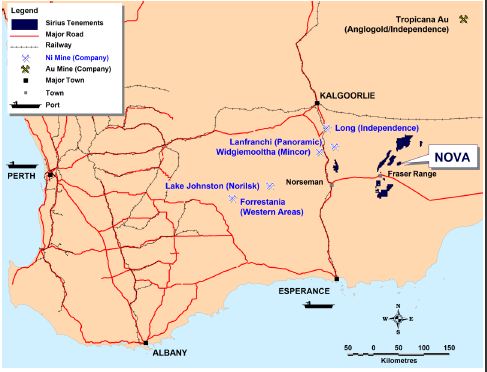

Nullagine Joint Venture location map.

The company has long-stated it has a modelled a three tiered business development strategy and it is determined to stick to it.

The first tier involves extending the known resources at the Nullagine JV, which is classified as Project Inventory.

“That means being fully informed as to what we have got and what we can mine down to every single tonne,” Young said.

“Our workforce is constantly working on developing that and we expect to deliver those results in the third quarter of this current financial year.”

The second tier to BC Iron’s strategy entails seeking out new opportunities to work with FMG.

“It’s pretty simple,” Young continued.

“They have a railway, we have a relationship, we know how they work, and they know how we work.

“Great; let’s go look at other projects.”

The third tier is the deal with Cleveland, which allows BC Iron scope to pursue projects in Brazil.

The deal is consistent with the ethos behind the BC Iron strategy in that it allows the company a very low cost entry into Brazil.

It also leverages off Cleveland’s vast intellectual property as well as the healthy amount of goodwill that company has built up during the past three years of operating in the country.

Cleveland recently completed a placement of approximately 16.9 million new ordinary shares raising approximately $10.7 million before costs.

BC Iron put its hand up for approximately 8.8 million of these at the price of 64.2 cents per share at a cost of approximately $5.64 million, representing five per cent of the total ordinary shares Cleveland will have on offer once the placement has been finalised.

“We took a placement in Cleveland as a good investment,” Young said.

“We decided that if we are going to work with these guys we may as well back them.

“It tells the market we support them, and it also tells Cleveland that we support them.”

With all the goodwill and cash in place, all the newly formed JV needs is a project to develop.

The intention now is to set up a Joint Venture committee to run its collective eye over a number of targets that are already under consideration.

“The Joint Venture committee will go and assess those targets, come up with drilling programs, assessment programs and co-fund it all,” Young said.

“We have formed a Joint Venture with a good company with very good management to operate in a good mining jurisdiction.

“All we need now is the right project.”

BC Iron Limited (ASX:BCI)

…The Short Story

HEAD OFFICE

Level 1

15 Rheola Street

West Perth WA 6005

Ph: +61 8 6311 3400

Fax: +61 8 6311 3449

Email: info@bciron.com.au

Web: www.bciron.com.au

DIRECTORS

Tony Kiernan, Mike Young, Morgan Ball, Terry Ransted, Andrew Haslam, Malcolm McComas, Jamie Gibson

MAJOR SHAREHOLDERS

Consolidated Minerals 23.9%

Regent Pacific Group 23.1%

Henghou Industries 9.9%

SHARES ON OFFER

104 million

MARKET CAPITALISATION

$271.1 million (at 23/8/12)