Altura receives 18 per cent increase to Mt Webber estimate

THE BOURSE WHISPERER: Altura Mining has received an increase to the Ore Reserve estimates for the company’s Mt Webber Joint Venture Direct Shipping Ore project located in the Pilbara region of Western Australia.

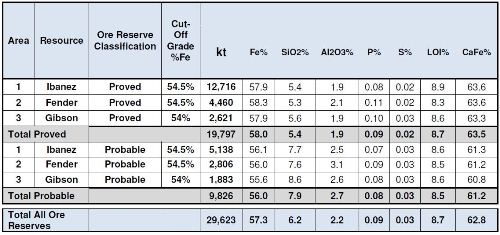

The new revised Ore Reserve estimate stands at 29.7 million tonnes of DSO at 57.3 per cent iron and replaces the previous estimate of 25.2 million tonnes of DSO at 57.5 per cent iron.

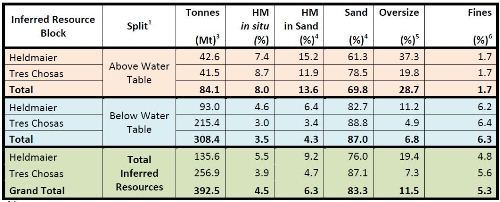

Mt Webber JV Ore Reserves (as at 30 June 2012). Source: Company announcement

The JORC compliant Ore Reserve estimate was compiled by the JV managing partner Atlas Iron and represents an 18 per cent increase to the previous estimate released in August 2011.

The increase is the result of an infill and evaluation drilling program focussed on the Gibson and Fender deposits, which moved more material into the Proved Ore Reserve classification.

An independent review of Atlas Iron’s Ore Reserves, including the Mt Webber JV deposits, for which a separate review was undertaken in isolation, highlighted the potential for an additional 35 per cent of reserve inventory with the inclusion of the lower grade ore within the pits.

“The addition of this material would require a reduction in the cutoff grade and marketing of a product marginally below the 57.5 per cent iron product (planned by Atlas) to 56.3 per cent iron,” Altura Mining said in its ASX announcement.

“Altura will recommend that a further review be undertaken to upgrade the Mt Webber reserves in Altura’s tenement with a lower cut-off grade of 50 per cent iron as was applied to the resource estimate.”

The Mt Webber DSO project is earmarked to be the main feed source for Atlas’ North Pilbara Horizon 1 development and is planned to commence production in late 2013.

“Altura has had continued discussions with Atlas in order to progress and finalise the Joint Operations Agreement (JOA) for the development and mining of the Mt Webber JV deposit,” Altura said.

“The negotiation and signing of the JOA (and associated commercial terms) is a prerequisite to allow both parties to arrive at a unanimous decision to mine the tenement and will provide Altura with a market access point for its share of the DSO production.”

Atlas is currently planning initial production at the rate of 3 million tonnes per annum (Mtpa) then rapidly ramping up to 6Mtpa from Mt Webber providing Altura with a 0.9Mtpa to 1.8Mtpa share of the annual production.

The production of 3Mtpa to 6Mtpa represents 40 per cent of the planned 15Mtpa production from the Horizon 1 area.

Disclaimer: The Roadhouse holds shares in Atlas Iron