Australian Bauxite: the company name says it all

With its first Tasmanian mining lease well on the way to being granted, Australian Bauxite (ASX: ABZ) is poised to take advantage of favourable developments in the global bauxite market.

Australian Bauxite’s (ABx’s) carefully planned success began in 2006 when chief geologist Jacob Rebek started looking for bauxite deposits on the eastern seaboard of Australia.

Rebek’s discoveries and enthusiasm enticed Ian Levy to join ABx as managing director in 2008, who brought with him a wealth of bauxite project development experience from his time employed with CSR and WMC in Western Australia and Aurum in Fiji.

Then, in 2009 the Indonesian Government passed a raft of laws to preserve the country’s limited bauxite resources for its own domestic industry, which it is now in the process of implementing.

“ABx floated in 2009, specifically to get a project up and running by 2014 to meet the foreseen peak demand,” Levy told The Resources Roadhouse.

“We are now on schedule to be shipping bauxite to customers in China toward the end of 2014.

“It really is credit to Jacob Rebeck; he recognised there was good bauxite in eastern Australia, near existing infrastructure in areas free of socio-environmental constraints.”

ABx secured core project areas along the Eastern Australian Bauxite Province extending from central Queensland, through New South Wales and Tasmania.

All 42 ABx tenements are 100 per cent-owned and free of obligations for processing and third-party royalties.

The company has discovered a number of new bauxite deposits and established global resources of 115.6 million tonnes of high-grade bauxite with a target of 200 to 300 million tonnes.

.jpg)

The Goulburn bauxite project in NSW has been advanced to pre-feasibility status and the Binjour bauxite project in Central Queensland is anticipated to soon follow.

However, it is from the 5.7 million tonnes already defined at the company’s Tasmania-based projects its first shipments of bauxite will be produced.

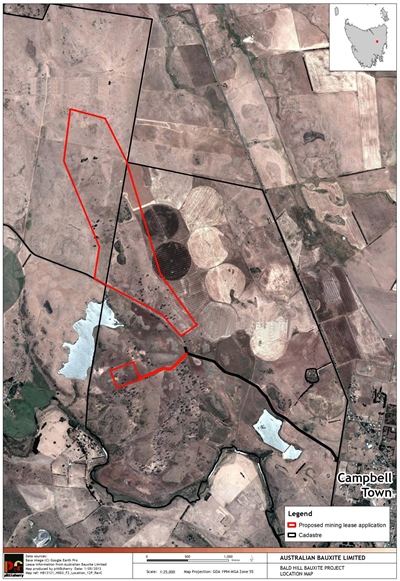

ABx’s first bauxite project development is now underway at Bald Hill, close to Campbell Town in the central northern Midlands of Tasmania, an area historically known for farming, quarrying, timber and industry.

“The response we have received from all avenues has been very positive,” Levy said

“We have consulted with all of Tasmania’s political players, local councils, and the local opinion-setters and all of them have said we have chosen the site to commence our operations very well.”

Selection of the site for ABx’s first bauxite mine wasn’t simple with 20 prospective sites to choose from.

“We didn’t know for certain which would be the easiest to get started and which would be the most difficult,” Levy said.

“Pitt and Sherry engineers went through every one of our discoveries and said Bald Hill was the easiest site to get started.

“So, having chosen the site carefully, we will now demonstrate how quickly the land can be rehabilitated – and we honestly believe we will leave the land in better than condition that how we found it.”

The significant aspect of Bald Hill and ABx’s other deposits is the Gibbsite-rich type of bauxite they possess, with elevated iron and also very low in reactive silica which is the main deleterious element in bauxites worldwide.

“It doesn’t have any boehmite which is a refractory mono-hydrate alumina,” Levy explained.

“With alumina minerals – there are two types – one is a tri-hydrate where there are three water molecules per molecule of alumina – and that’s called Gibbsite.

“For example, Western Australian bauxites are Gibbsite rich, they are the lowest grade bauxite deposits being exploited in the world – by a long away – yet they are by far the lowest cost producer of alumina because Gibbsite bauxite is more easily refined at much lower temperatures.”

Another important facet of Gibbsite bauxite is its current in short supply world-wide.

This shortage has been intensified by Indonesia, which has long been a major source of bauxite for China and implemented the first of two major cutbacks to exports in mid-2012.

Indonesia closed a dozen mines and imposed a 20 per cent export tax on bauxite.

In 2014 Indonesia is expected to shut more mines and increase export tax to 50 per cent.

As Indonesian imports wane, China’s demand for seaborne bauxite grows, especially as its own domestic bauxite is deteriorating in quality and rising in cost faster than analysts had predicted.

Chinese bauxite imports reached an all-time monthly record of 6.3 million tonnes in May 2012 then fell to one million tonnes in June 2012 after Indonesia’s first round of bans took effect.

Since then they have has steadily returned to between four and five million tonnes per month, which is insufficient for China’s demand.

“China is looking more and more at importing bauxite from the Asia-Pacific area with Australia emerging as the most logical provider,” Levy said.

Earlier this year, ABx executed a Term Sheet with major Chinese aluminium company, Xinfa Group in regards to early development and operation of the company’s Tasmanian and Goulburn South bauxite projects.

“Xinfa is the second largest importer of bauxite into China, importing more than 10 million tonnes per year,” Levy said.

“We anticipate initially supplying Xinfa with one million tonnes per annum and, hopefully growing that to more than three million tonnes per annum.

“2014 will probably see similarly high prices and we hope to lock-in a few million tonnes with a large operating profit margin.”

Levy compared the likely 2014 Indonesian bauxite prices, which are due to rise through it increasing export taxes and will cost more than US$63 per tonne Cost Insurance and Freight (CIF) to ABx’s proposed cost figures.

“Our operating expenditure looks like being less than US$27 per tonne Free On Board plus US$19 per tonne shipping for a total of approximately US$46/tonne CIF to China,” he explained.

“We are likely to sell at above Indonesian and Indian bauxite prices with operating margins of $10 to $20 per tonne.

“We hope to start at 750,000 to 1,000,000 tonnes per annum and grow to about 3 million tonnes.

“Eventually, we hope to develop a five million tonnes per annum project out of Binjour in Central Queensland via an expanded Bundaberg Port in 2017 onwards – to be our flagship project.”

Bauxite has undergone a ‘quiet revolution’ in recent times.

One contributing factor to this has been the fall in seaborne bulk transport costs, bringing Australia closer to Asia than ever before.

In 1975, it cost US$35 per tonne to ship bulk to North Asia, or US$150 per tonne in today’s money.

Today, the same shipment will cost US$18 per tonne – about 10 to 15 per cent of what it once cost.

“This is a technological revolution that has not been noticed by the investment community – Keating was wrong; we are not at the arse end of the world,” Levy said.

“Similarly, aluminium production costs have benefited from major advances in smelting technology – and real costs of aluminium metal are falling faster than for all other significant metals.

“This means consumption of aluminium will rise faster than other metals as aluminium becomes increasingly cost competitive in transport, power, construction and consumer goods.

“The net effect will be consumption of aluminium will keep rising, leading to the demand and prices for seaborne bauxite to keep rising strongly.

“Australia is poised to be the main beneficiary.”

Australian Bauxite Limited (ASX: ABZ)

…The Short Story

HEAD OFFICE

Level 2

131 Macquarie Street

Sydney NSW 2000

Ph: +61 2 9251 7177

Fax: +61 2 9251 7500

Email: corporate@australianbauxite.com.au

Web: www.australianbauxite.com.au

DIRECTORS

John Dawkins, Peter Meers, Ian Levy, Jacob Rebek, Wei Huang, Ken Boundy

MAJOR SHAREHOLDERS

Hudson Resources Limited 28.73%

Gleaneagle Securities 9.68%

State One Stockbrokers 7%

Washington H Soul Pattinson5.5%

SHARES ON ISSUE

114 million

MARKET CAPITALISATION

22.2 million (9/05/13)