When governments are stealing your savings, gold is the only option

GAVIN WENDT: Over the past few weeks we’ve focused our commentary exclusively on gold. The reason is simple – no other commodity is currently exposed to the same level of misrepresentation or misunderstanding as the price of gold bullion. We’ve seen all sorts of traders and experts talking down gold’s prospects, based on recovering sharemarkets and supposed economic growth.

As we’ve discussed over recent weeks, most of this can be dismissed. The US economic strategy (which ironically is the same methodology that caused the mess in the first place) is to pursue easy credit, obscenely low interest rates and a race to the bottom as far as their currency is concerned.

Ironically, Japan is also following suit – despite the fact that the same failed economic policies have left it an economic basket case since the 1990s. And ironically too it is the USA, which has been one of China’s toughest critics in terms of its supposed ‘currency manipulation’, which is now manipulating its own currency for short-term political ends.

The scary part is that the average US citizen’s lot has not improved despite the tens of trillions of dollars poured into the nations’ monetary system since 2008 – in fact, by virtually all measures (net income, purchasing power and investment returns) – they’ve gone backwards. So the health of world sharemarkets in no way reflects the strength of the underlying world economy.

Americans, on average are making less money, are less wealthy and are not nearly as monetarily comfortable as they were five years ago. The only other explanation for the recent increase has to be overall economic growth, but it isn’t. The US economy has grown since late 2007, but at an extremely weak rate. Inflation-adjusted (or real) GDP is about 2.5 per cent higher than it was in October 2007, but when annualized it represents an extremely modest growth rate of just 0.5 per cent.

This represents a rate of growth which is lower than the population growth rate over the same timeframe. And since 2007 the US national debt has risen by 83 per cent within a period of just 5 years. So the argument that the US is doing well is a difficult one to swallow.

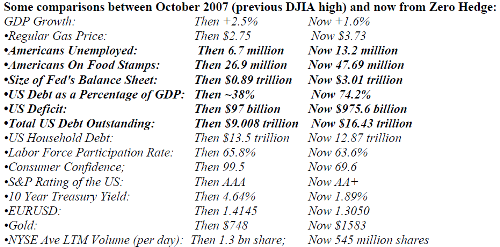

The situation is best illustrated by the stark statistics supplied by Zero Hedge:

This brings us back to gold. The arguments against the precious metal in the current context are flimsy, but we’ve seen them made several times (notably during 2006 and 2008) during the latter half of gold’s 12-year bull-run since the year 2000. The so-called experts of course proved to be wrong on each occasion, with gold quickly recovering and reaching new highs.

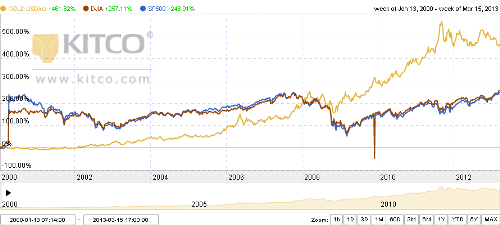

And I’ve no doubt that the current situation isn’t any different. I stated months ago that despite the bad press gold was getting and its declining price, I would be surprised if gold didn’t rebound to its long-term support level around US$1,600 – which is almost exactly what’s it’s managed to achieve over the past fortnight. And over the past decade gold is still shown to be outperforming the Dow Jones and the S&P 500 Indices.

So despite all the money that the US Federal Reserve has printed and pumped into the system, over the last five-and-a-half years the Dow Jones has not provided investors with a return. Think about it – the Dow has just gotten back to where it was back in October 2007 and many investors are still struggling to make up their losses following the GFC that wiped out $37 trillion from global equity values. By contrast (and despite prices falling over the past two years), over the last five years gold has provided a return of approximately 120 per cent.

The reasons for gold’s recent recovery are all related to big question marks over the supposed ‘economic recovery’ that’s taking place within both the European and US economies. Gold has just capped its longest rally in six months on the back of indications of slowing growth in Europe, which in turn could lead to central banks further expanding stimulus measures.

Data has shown that UK industrial production unexpectedly fell during January compared to the previous months, whilst a US government report showed that unemployment continues to remain above the target set by the Federal Reserve, signalling the central bank will continue stimulus measures. The US jobless rate dropped to 7.7 per cent, but is still well above Fed Chairman Ben Bernanke’s target of 6.5 per cent.

And in probably the best example (or worst, depending on your perspective) of how Europe’s economic and political turmoil is far from over (in fact it could be about to get a whole lot worse), European officials in Brussels recently announced that they will require that part of a new 10 billion euro bail-out to Cyprus be paid for directly from the bank accounts of ordinary citizens. Ordinary people were to be forced to have 10 per cent of their bank savings seized – in a program that can best be described as thievery by the state.

As The New York Times reported, “In a move that could set off new fears of contagion across the euro zone, anxious depositors drained cash from automated teller machines in Cyprus on Saturday, hours after European officials in Brussels required that part of a new 10 billion euro bailout be paid for directly from the bank accounts of ordinary savers.”

And little wonder. The terms of the deal, which imposed a charge of up to 10 per cent on savings accounts, breaks a previous taboo of protecting depositors. The move has raised questions about whether bank runs could be set off elsewhere within the euro zone.

Under an emergency deal reached in Brussels, a one-time tax of 9.9 per cent is to be levied on Cypriot bank deposits of more than 100,000 euros effective from Tuesday, hitting wealthy depositors – mostly Russians – who have put vast sums into Cyprus’s banks in recent years. But even deposits under that amount are to be taxed at 6.75 per cent, meaning that Cyprus’ creditors will be confiscating money directly from pensioners, workers and regular depositors to pay off the bailout tab.

Not surprisingly, people around the country have reacted with disbelief and anger. “This is a clear-cut robbery,” said Andreas Moyseos, a former electrician who is now a pensioner in Nicosia, the capital. Iliana Andreadakis, a book critic, added: “This issue doesn’t only affect the people’s deposits, but also the prospect of the Cyprus economy. The E.U. has diminished its credibility,” he told CNBC.

Sharon Bowles, a British member of the European Parliament who is the head of the body’s influential Economic and Monetary Affairs Committee, said the accord amounted to a “grabbing of ordinary depositors’ money,” billed as a tax. “What the deal reflects is that being an unsecured or even secured depositor in euro-area banks is not as safe as it used to be,” said Jacob Kirkegaard, an economist and European specialist at the Peterson Institute for International Economics in Washington. “We are in a new world,” she told CNBC.

And let’s not forget Italy. Recent elections have left Italy facing its worst recession since World War II. Fitch Ratings has lowered Italy’s sovereign rating to BBB+ from A- with a negative outlook. Across the Euro zone, youth unemployment increased to 24.2 per cent during January, up from 21.9 per cent during the same period a year earlier. In the EU, under 25-year old unemployment rose to 23.6 per cent from 22.4 per cent, whilst in Greece the youth unemployment rate was around 59.4 per cent, with Spain at 55.5 per cent and Italy 38.7 per cent.

Unemployment numbers in France rose also by 43,000 during January to 3.16 million, an increase of 10.7 per cent from last year. The figure is at its highest since January 1997, when it reached 3.19 million.

As we’ve commented previously, the sensible investor understands that gold’s recent price drop does not alter the long-term picture. I remain bullish on gold and believe that after a period of consolidation around its long-term support line at US$1,600, it will inevitably push higher.

As noted gold industry expert David Levenstein said last week: “Despite the negative sentiment and downward pressure on gold, I remain extremely bullish. While I am fully aware recent trading has been particularly turbulent and incongruous as the price of gold continues to trade mostly lower, I simply see no reason to panic and sell one single ounce. And, I firmly believe that the upside for the yellow metal is far greater than the downside. And, even though most of the dire outcomes predicted for paper money have not materialized, central banks around the world are diversifying some of their paper currencies into gold.”

“One of the main reasons people invest in gold is not to speculate, but to protect one’s wealth against what may happen in the future. By buying gold you have something of intrinsic value instead of a paper currency which could become totally worthless. Owning physical gold is like taking insurance against your government and the financial system. And, right now, no matter what the main stream media may tell you about an economic recovery, gold is something you should buy because you cannot trust your government or central bankers.”

So whilst gold has recently been at an eight-month low, and as most of the major investment banks have turned bearish on gold, the precious metal has staged yet another recovery. The reason for my positive outlook on gold relates to the fact that the fundamental drivers for investing in gold have not altered, and as the people of Cyprus are finding out, we are silly to put our trust in any government. Instead, the better option is to invest in gold.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report