Uranium: more supply shut-downs inevitable

GAVIN WENDT: Despite the hit that the uranium business initially took with respect to sentiment in the wake of the Fukushima earthquake back in 2011, the conundrum remains the same: the world has few alternatives in terms of substantial, reliable base-load power generation.

Realistically, in a world with burgeoning populations in emerging countries and an escalating need for energy, there will be even greater demands placed on all three forms of traditional energy – coal, gas and nuclear.

The Fukushima nuclear disaster made the world take a second look at the safety of nuclear energy and many countries halted construction and plans to build nuclear reactors.

Japan shut down all but two of its 50 nuclear reactors in the wake of Fukushima.

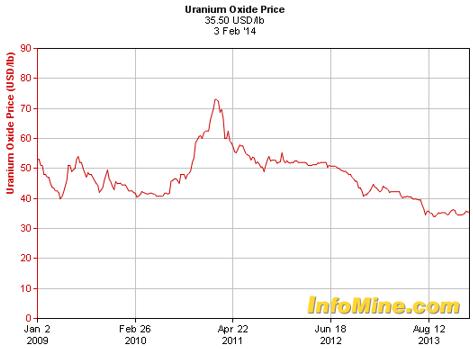

As a result, uranium prices have been in free-fall ever since. However, there are a number of strong catalysts for future uranium producers.

For starters, there are very real supply challenges being faced by the nuclear industry, driven by two very important considerations.

During 2013, the world’s 435 current nuclear power generators are expected to require 20 per cent more uranium than was currently being produced from the world’s mines.

Power generators will need more than 66,000 tons of uranium, but current global mine production is just 55,000 tons.

Over the past 20 years, the effective supply gap has been alleviated by uranium from decommissioned Soviet-era nuclear weapons.

During 1993, the United States signed an agreement with Russia called ‘Megatons to Megawatts’.

The agreement was a 20-year program where Russia down-blended the equivalent of 20,000 nuclear warheads to produce more than 14,000 metric tons of low-enriched uranium.

This uranium supplied the United States with nearly half of its nuclear generated energy over the past two decades, which is almost 10 per cent of the country’s total electric needs.

The final shipment from this program arrived in Baltimore on December 10, 2013, marking the end of the agreement.

To make up for the end of this supply of uranium coming to the US, USEC signed a 10-year agreement with Russia’s Techsnabexport (TENEX) to provide USEC with Russian enriched uranium.

However, this agreement will only supply half of the uranium previously supplied under the Megatons to Megawatts program and won’t reach that level until 2015.

This new agreement won’t come from down-blending nuclear warheads, but rather from Russia’s commercial enrichment activities.

During 2013, US nuclear plants required 19,622 metric tons of uranium.

Taking into account the end of Megatons to Megawatts and the new agreement between USEC and TENEX, there will have to be 4,000-5,000 metric tons of uranium coming from new sources during 2014 and beyond.

The Fukushima nuclear disaster in Japan has merely delayed the onset of the upcoming supply crunch, but it is entirely real and power station owners and governments will be increasingly nervous.

An additional supply challenge relates to the lack of investment in the uranium sector, which bears a direct correlation with two important factors: firstly, low uranium prices provide a disincentive to commission new uranium supplies; and secondly, depressed conditions in equity and lending markets over recent years make it extremely difficult (if not impossible) to source funding for new uranium developments.

Significantly too, even the major players in the uranium business that have the balance sheet strength to finance their own developments (without having to rely heavily on outside funding sources) are leaving new sources of supply undeveloped in most instances.

Quite simply, where is the incentive to bring new supply on stream when prices are already painfully low?

This illustrates the fundamental discrepancy within the uranium industry relating to where prices realistically should be (i.e. reflective of the looming supply shortfall) in order to stimulate profitable new levels of production, and where they currently are (i.e. trading at depressed levels and acting as a major deterrent to new project investment).

Nowhere is this more pronounced than at the smaller end of the uranium business.

At current prices there is an enormous amount of strain placed on uranium producers, to the point where the majority of existing operations would be barely breaking even around the $35 per pound mark, so prices below this level aren’t sustainable.

This is clearly evident in the fact that Paladin Energy (ASX: PDN) has announced it is suspending production at its Kayelekera mine in Malawi, placing it on care-and-maintenance to preserve the orebody until a sustained recovery in uranium prices.

Paladin blamed the continued depressed uranium price for the closure.

The silver lining in all of this is that the medium to longer-term fundamentals for uranium are strong.

New mines will be required and prices will inevitably have to rise in order to allow this to happen.

Looking ahead, uranium prices upwards of $70 per pound will be necessary in my view to justify and support investment and development of new projects.

Gavin Wendt is the founder of Minelife, publisher of the MineLife Weekly Resource Report