The irrationality of gold’s recent price performance

GAVIN WENDT: In a further demonstration of the irrationality of financial markets at present, the price of gold fell sharply over the past week, despite a host of supporting factors that under normal circumstances would result in a stampede towards the precious metal.

Recently, we’ve witnessed a ratcheting-up of the rhetoric from the rogue state of North Korea, more poor economic news emanating out of the United States of America, and a host of deteriorating economic indicators out of Europe – all of this hot on the heels of the Cyprus bail-out.

As we’ve discussed over recent months, I’ve long since given up trying to make sense of the current international economic picture.

What I am increasingly confident about however with every passing day is the importance and relevance of gold in both the current and future financial landscape, despite the complacency and overconfident nature of the rhetoric that seems to accompany the current economic landscape.

I have little confidence in the supposed economic recovery in the USA. It’s in reality a ‘modest’ recovery at best, which in no way bears any relation to the booming US sharemarket – which is essentially a market that’s been pumped up to the max on Fed-administered financial steroids.

If you pump trillions of dollars into a financial system then of course you’ll generate growth – but there are serious consequences.

The problem is that the US has mortgaged its future by bringing forward future consumption in a desperate attempt to try and stave off a deep and prolonged recession.

Worryingly, this might still happen, as the US sharemarket in no way reflects the enormous underlying problems inherent within the economy.

More US citizens are living on food stamps, the labour participation rate is falling, home affordability is declining, living standards are deteriorating, the divide between rich and poor has never been greater, and peoples’ savings are being wiped out by ultra-low interest rates.

In an attempt to drive its stuttering economy forward, the US Government is once again venturing down the same dangerous path of providing cheap funding, whilst at the same time devoting little attention to the credit worthiness of the borrower.

According to most mainstream financial media and market experts, risk is being reduced and the US is leading a global economic recovery.

As a result, gold is being viewed by many as an unnecessary insurance policy, thus falling to a 10-month low of $1,540 per ounce.

A total of $9.7 billion has been sold from exchange-traded products since the record high reached on 20 December 2012, whilst hedge funds have reduced their bets on higher gold prices by 70 per cent since October 2012.

We’ve also had a host of banks and brokerages this week calling an end to gold’s 12-year run.

What’s interesting though is that whilst brokers, bankers, traders and speculators might be abandoning gold, true investors aren’t.

Central banks added 534.6 tons of gold to their reserves last year, the biggest surge in gold buying since 1964, whilst gold coin sales in the US remain robust.

Why gold should benefit from rising interest rates

What’s interesting is that over the past five years, a lot of popular theories relating to the demise of gold have been proven false.

A popular theory during 2009 was that a ‘green shoots’ recovery (remember that term?) would cause gold prices to collapse. Well they didn’t.

Then there was the popular ‘contrarian’ argument that the real threat was deflation, and that gold would sell off as a result.

Gold once again rose, instead of falling. Now it’s the notion that rising interest rates will kill off gold.

One of the major reasons cited by commentators and financial experts for gold’s recent sell-off has been a prevailing view that interest rates will rise as economic growth begins to build.

There is a view held in many quarters that a rising interest rate environment is bad for gold.

Whilst I firstly have a major question mark over the whole concept of sustained economic recovery, let’s assume for the moment that they’re right and that interest rates will rise in accordance with economic growth.

Why shouldn’t gold benefit from a rising interest rate environment, just as it has done in a low interest rate environment since 2008? Let’s examine the evidence of recent history.

Significantly, gold rose with interest rates during the 1970′s and this is sufficient to prove that gold doesn’t always fall with rising interest rates.

For a good modern day example that pertains closely to the current economic situation, let’s examine Greece.

The nation is experiencing massive unemployment, wage deflation and rising interest rates, yet gold is hitting new highs as Greeks have flocked to gold.

Accordingly, a few myths have been destroyed: firstly that gold rises with inflation; and secondly that gold falls with rising interest rates.

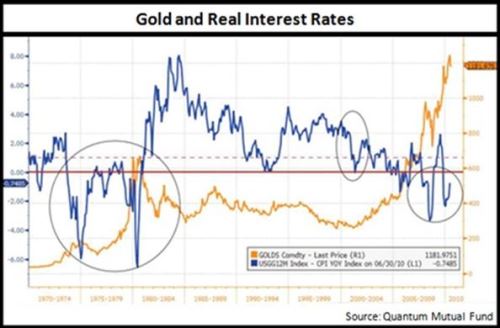

The real driver of gold prices is negative real interest rates (defined by nominal interest rates minus inflation).

Central bank policies of inducing negative real rates to ‘incentivize’ borrowing, expanding the money supply, and devaluing currencies – have forced investors (especially mums and dads) into real assets like gold and silver.

Debt is inherently inflationary if you have the ability to print your own currency.

As the chart below highlights, it’s happened before.

In a gold bull market that has been fueled by negative real rates, conventional thinking would suggest rate increases would, at the very least, halt the rise of gold as the negative real rates get closer to turning positive.

History however actually says the exact opposite is true.

The gold bull market of the 1970s was dominated by inflation. Interest rates rose steadily to keep up with it, but real interest rates were mostly negative the entire time.

Peaks in gold prices since 1975 have usually been associated with rising real interest rates.

Times when real interest rates fell in tandem with gold prices include 1987-1990 and 1996-2001.

Even though real rates are have risen slightly, they remain below their historical average and levels below 2 per cent have still been supportive of rising gold prices.

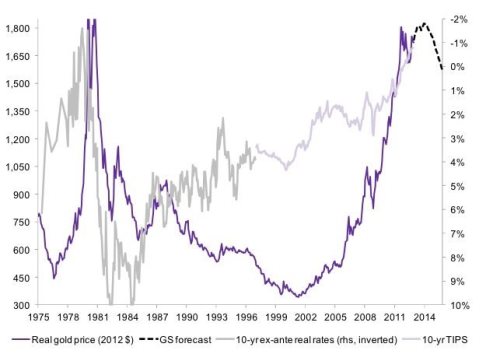

As the chart below from Goldman Sachs demonstrates, gold prices languished from 1980 to 2000 and had declining correlations with debt levels, because GDP growth was sufficient to mute fears about budget and deficit issues.

The current economic recovery has been too weak to support a sustained rise in real rates above the 2 per cent level that has acted an inflection point for gold prices.

With energy and food inflation deepening and soon to affect consumer price indices, interest rates may have to rise significantly in order to restore real interest rates above 2 per cent.

This is exactly what ex Federal Reserve Chairman Volcker did during the late 1970′s, when he increased interest rates above 15 per cent in order to protect the dollar and aggressively tackle inflation.

It is unlikely that similar ‘hawkish’ monetary policy would be implemented by the Bernanke Fed today.

It is unlikely that they would and even doubtful if they could – given the appalling fiscal situation and levels of debt in the US and global economy.

As a result, I retain every confidence that we will ultimately see higher gold prices.

I believe that the US$1,600 per ounce mark is still a strong near-term support level and that prices will rebound even if we see further near-term price weakness.

Private investors and central banks are buying gold in strong volumes, as they rightly have little confidence in the world’s major currencies.

Economic circumstances in Europe and the US are set to deteriorate and gold will be the biggest beneficiary.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report