Key factors pointing to a resources sector turnaround

GAVIN WENDT: If one looks at long term charts of most metal prices, one sees a very distinct cyclical pattern. When commodity prices are high this stimulates new mine development, but unfortunately it is the nature of things that new mines tend to come on stream at or around the same time. As a result, commodities move into surplus and prices retreat.

This is exactly what we’ve witnessed in the resources space over the past couple of years. Profitability has fallen, uneconomic operations have been closed down (some unlikely to ever reopen) and global production has stalled. But things are beginning to turn – commodity prices in many instances are rising and the resources cycle is beginning to repeat itself.

Most mining companies and sophisticated resources investors comprehend this process well, although a prolonged period of high metals prices (as we saw during the recent boom) often means that this basic premise is forgotten. The short-termism of the financial community also helps compound the process – providing a barrage of funding for all sorts of questionable resource plays during boom times, then slashing financing immediately times turn bleak.

The essence of the resources boom is this: stock prices rise as miners make larger profits; institutional shareholders press for more production (which they see as leading to ever higher returns); banks make lending easier for building of new operations; high stock prices make raising equity capital easier; and miners get carried away in the general euphoria.

The upshot is that many horrendously expensive new projects get commissioned as operating costs escalate out of control – in essence, growth for growth’s sake. Suddenly miners find themselves on the back foot – just as we’ve seen over the past couple of years.

Profits and share prices have fallen, and the same shareholders that were previously calling for expansion are now calling for cost reductions and output restrictions. As a result capital projects are either deferred or cancelled, and exploration expenditure is slashed. Further down the food chain things are even worse with most juniors and mid-tier companies cutting expenditure in a battle for survival until prices start to rise and the cycle begins again.

This is why I am confident that we are starting to see the beginnings of the next resources cycle. There are enough important factors that have emerged over the past few months that indicate that this is so.

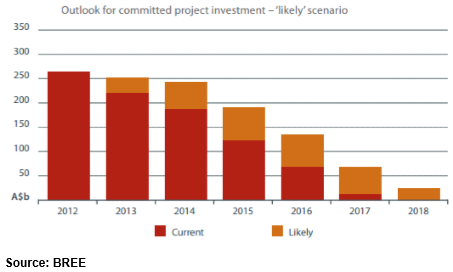

1. Supply side cutbacks are beginning to bite

Supply side factors are set to have a major impact on commodity prices. As the chart below highlights, resource companies have slashed their level of committed projects dramatically as a result of lower commodity prices, rising costs, funding difficulties and shareholder pressure. These factors will in turn hasten the onset of the recovery, as future supply restrictions will mean higher commodity prices.

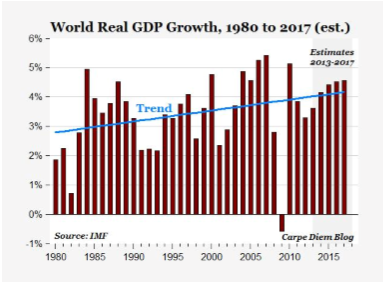

2. Growth figures are encouraging

Global growth is beginning to recover – China is still growing at around seven per cent a year, there’s modest growth in the US, and even Europe is showing some signs of life. The outlook for world economic growth in the chart below paints a quite positive picture. Uncertainty about the potential longevity of monetary stimulus has taken some of the shine off risk appetite, but global central banks should continue to provide support given the global recovery is nowhere near being self-sustaining.

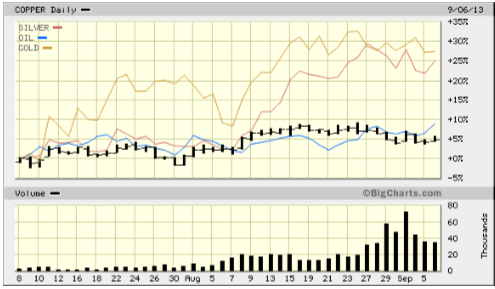

3. Commodity prices are recovering

Bullish sentiment for commodities (particularly cyclically sensitive sectors) has picked up over the past month, as indicators of economic activity from China and the Eurozone continue to improve. Several key commodities are performing well over recent months – oil, gold, silver, iron ore and copper. Steel production levels remain solid and iron ore prices are defying gravity.

After a difficult start to the year for commodity markets, demand conditions are becoming more favourable and prices are beginning to reflect the strength of the global recovery. Outside of the agricultural sector, rising supply tightness will continue to be a key trend that provides price support.

The energy and metals sectors will be the main beneficiaries from concerns over reduced production. South African labour developments for platinum group elements, along with unrest in the Middle East and North African regions for the crude market, are the key upside price risks that investors will primarily be focusing on.

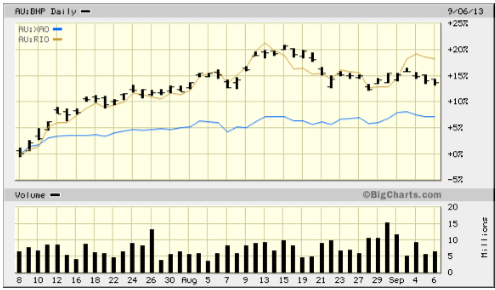

4. Sector heavyweights BHP and RIO are performing solidly

Any potential recovery in the resources sector always begins with the sector heavyweights. There’s been a steady flow of funds into ‘cheap’ sector heavyweights BHP Billiton and Rio Tinto over the past couple of months, as investors have moved away from the high-yield plays in the industrial space (particularly banks) over the past two years.

This is reflected in the robust share price performances of both companies in the chart below, as they have outperformed the All Ordinaries Index. Over time, funds will trickle down to the mid-caps and junior sector, and as a result access to badly-needed exploration and project funding will improve.

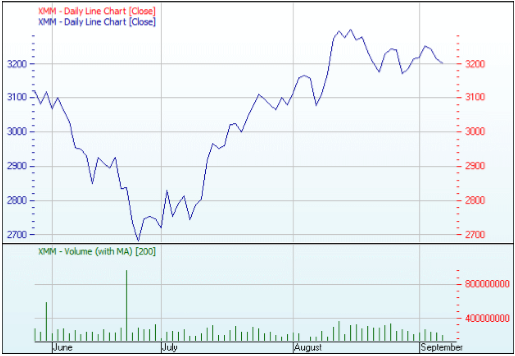

5. Bargain hunting following EOY tax-loss selling

The chart below highlights the decline in the ASX 300 Mining Index during the latter stages of the previous financial year, followed by a subsequent strong rebound. This is not surprising, as tough markets often result in a ‘clean out’ of underperforming stocks on the part of investors as part of tax-loss selling prior to 30 June.

This also provided the opportunity for sophisticated resources investors who had been eyeing discounted, high-liquidity stocks for some time to dip their toe in the water and begin accumulating. In my view, this accounts for the robust recovery that we’ve seen in the resource equity market since late June to the present.

6. Change of Government

The Coalition’s win in the recent Federal election should provide a significant boost for resources investors and junior exploration companies in particular. The first reason is change – the market is looking for some sort of catalyst that might provide a boost to sentiment – and a change of government might just provide it.

The second reason for optimism is the Coalition’s desire to implement a flow-through taxation scheme, which would enable a ‘flow-through’ of companies’ exploration expenses to investors in the form of a tax credit. The Coalition said it would allow investors to claim tax deductions on share investments in ASX-listed exploration companies from 1 July 2014.

Known as the Exploration Development Incentive, it would allow investors in mineral exploration companies to claim tax deductions against their investment in companies which were involved in exploration, and which accrued relevant deductible expenses. It would also ensure that the system is not open to abuse by non-genuine exploration investing or rorting.

Finer points of the plan are expected to emerge now that the election has been run and won, but it is expected the scheme will target small exploration companies by limiting eligibility to companies with no taxable income, and will be capped at $100 million over the forward estimates. The plan should stimulate investment in exploration over the next three years.

The plan should provide a strong incentive for investors and shareholders to commit capital to the exploration sector, making investment in small cap explorers attractive again. It should also play a part in helping boost the rate of resource discovery and provide future revenue from the mines of tomorrow.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report