Ignore the skepticism – the outlook for copper remains robust

GAVIN WENDT: In Rio Tinto’s March quarter production report released recently, it was evident that there are significant difficulties being faced by the company’s copper business.

Rio’s mined copper production was 18 per cent lower than the first quarter of 2011, due to anticipated lower grades at Kennecott Utah Copper.

I reiterate our position that this isn’t anything particularly new, as we’ve previously addressed the production issues afflicting many of the world’s major copper mines.

It’s these very same issues that reinforce our positive view on the outlook for copper prices.

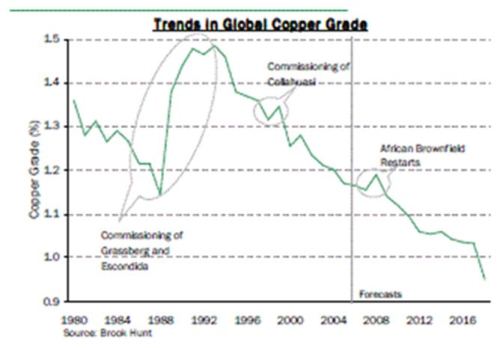

Copper head grades are declining alarmingly at virtually all of the world’s major copper mines, forcing up production costs, which in turn are impacting significantly on world copper supplies.

In fact, the average head grade at the world’s major mines has fallen by around a third over the past decade, meaning miners have to mine a third more ore (at significantly higher cost) just to maintain production levels of a decade ago.

And it’s not just a recent phenomenon, as the graphic below clearly demonstrates.

From a demand perspective copper has long been regarded as the bellwether commodity of international economic growth – and rightly so, as it’s used extensively in everything from homes to motor vehicles to electronics.

Despite comments over recent times predicting significant price falls based on weakening demand, copper’s fundamentals in my view remain robust.

This supports my bullish argument that the copper market will likely see another deficit during 2012 as existing operations struggle, whilst new projects are still a year or two away from making a significant contribution.

And one of the best case studies is Chile, the world’s biggest supplier of the red metal.

As Bloomberg highlighted recently, “While the global copper market is nervously eyeing signs of slowing demand in China, tumbling ore grades, energy protests, extreme weather and labor unrest in top miner Chile were the focus of the annual CESCO conference.”

While Chile continues to produce a third of the world’s copper supply and holds an estimated 28 per cent of global reserves, the nation needs to address various fronts in order to boost annual output to the plus-seven million tonnes it’s aiming for by the end of the decade.

Joaquin Villarino, head of the country’s Mining Council that represents Chile’s biggest miners, said during a recent forum on energy, “We’re frankly at a very delicate moment, especially in terms of energy.

“If we’re not able to solve several problems, mining isn’t going to develop in the country or it will develop less than we would like.”

Of course, supply constraints are good news for prices.

With no significant deposits slated to come on-line this year, the so-called “strike season” yet to kick off in Chile, and both Xstrata and Rio predicting falls in their production during H1 2012, Chilean miners are predicting tight supplies will offset any Chinese slowdown.

Codelco, Chile’s state-owned copper producer has an ambitious plan to boost its annual output to 2.1 million tonnes by 2020, but forecasts a slight easing in production this year.

Chile is seen attracting $1 billion in mining investment through 2020, but some analysts have questioned that figure as overly upbeat.

Antofagasta Minerals last year launched its flagship mine Esperanza, or “Hope” in Spanish, one of the few promising deposits to come online in a copper market defined by its scarcity of new projects.

But Esperanza’s has so far disappointed in output terms, contributing to Antofagasta missing its 2011 copper output target.

As Bloomberg highlights, “Few deposits are more emblematic of Chile’s potential decline than its massive but tired, water-short and energy-strapped copper mines in the mineral-rich Atacama desert.”

A prime example is Codelco’s century-old Chuquicamata mine, which has seen its output drop from 528,000 tonnes in 2010 to 443,000 tonnes last year, chiefly due to declining grades.

Chuquicamata is set to undergo massive transformation to become an underground operation, whilst major expansions are planned at both Collahuasi, owned by Anglo and Xstrata, and Escondida, which is majority owned by global miner BHP Billiton.

Collahuasi is the world’s third-biggest copper mine and its output dropped during Q1 2012 on the back of weather disruptions and lower grades.

Meanwhile the world’s biggest copper mine, Escondida, saw its output plummet 25 per cent during 2011 due to a shock two-week strike and declining ore grades.

All of this should translate into a tight copper market during 2012, a view shared by Thomson Reuters GFMS’ Research director Sanjay Saraf, who this week predicted that supplies would remain constrained as factors that have impacted output in previous years continue to persist.

“Even factoring in increased mine supply, we are still forecasting a deficit for 2012 as a whole, albeit a smaller one than last year’s estimate of 256 000 tonnes,” he said.

Freeport-McMoRan chief executive officer Richard Adkerson expressed his view on a first-quarter earnings conference call that the fundamentals of the copper market remain strong, given China’s drive to invest in infrastructure projects and lower levels of inventory in the United States and Europe.

“Markets continue to be very positive this year for copper … 2012 appears to be another year of deficit in the copper market,” Adkerson said.

We retain a positive outlook on copper’s fundamentals and anticipate that prices will range between US$3.50 – US$4.25 during the course of 2012.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report