Will commonsense eventually prevail? Bigger is by no means better

One of the most common sense opinions I’ve heard expressed in the resources sector over recent times came from a North American mining company executive, James Hekseth, who in a presentation recently to a mining association conference panel discussion on mine financing, urged miners not to be pressured into building large mining projects in an effort to keep major investors and mining analysts happy.

James Hesketh is the president and CEO of junior resources play, Atna Resources, who in his commentary suggested that the mining industry is now suffering from an “insane drive for capital raising.”

According to his estimates, less than 25 per cent of mining projects actually get to the feasibility stage, whilst some mining companies are over-capitalizing ore bodies, essentially destroying their economic value by proposing projects that are too large.

“While others are looking for mega capital, we are starting small,” he stated.

Hesketh also urged emerging mining companies to “Stick to your knitting and build what you’ve got.”

Atna is a company that has concentrated on building value from its existing properties.

Atna plans to continue executing its strategy of developing advanced-stage growth projects using the cash flow from existing mines.

I know such comments would be music to the ears of Evy Hambro, the outspoken resources head of the world’s largest find manager, BlackRock.

The group has been harsh critics of mining companies, particularly the heavyweight miners (like BHP Billiton and Rio Tinto) and gold miners (like Barrick and Newmont), who they’ve accused of wasting money on acquisitions and not returning enough cash to long-suffering shareholders.

BlackRock has singled out the gold sector, which the group believes could end a period of dramatic underperformance by ceasing to chase volumes and instead improving returns to shareholders.

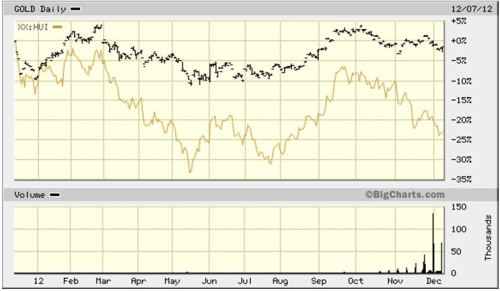

The evidence is compelling – the price of gold bullion has soared roughly 500 per cent since 2000 (from less than US$300/oz to around US$1,700/oz), but global gold equity prices have grown at just a quarter of that rate.

BlackRock has rightly pointed to production that has stagnated over the past decade, whilst project quality has deteriorated in the race for ounces.

“It is easy to blame Mother Nature, but… if you look at capital discipline in the industry, it has been appalling,” according to Evy Hambro at a recent London conference.

Most of the gold industry’s production growth since 2008 has come from up-and-coming players in emerging countries such as China.

Meanwhile, the established giants of the gold industry such as Barrick and Newmont have chased lower-grade supply for the sake of scale, whilst they’ve also used cost measurements that in my view don’t fully reflect the actual cost of production.

There is also the issue of poor dividends – the oil sector pays out 45 per cent of profit, whilst the gold sector pays out just 25 per cent.

The 16-member benchmark Arca Gold BUGS Index (which includes all North American heavyweight producers), has risen by 8.4 per cent since early 2008, whilst the price of gold has more than doubled over the same period.

Members of Arca Gold BUGS will pay an average 1.6 per cent dividend yield this year, which compares with an average 3.8 per cent for the STOXX Europe 600 and 2.5 per cent for the 140-member Bloomberg World Mining Index, despite the fact that gold prices have risen for 11 consecutive years.

Figure 1: Spot Gold Price v Gold Bugs Index – Courtesy BigCharts

One of the key factors in the underperformance is rising cash production costs (which are crimping margins) – the average cost per ounce of gold for large producers has advanced for nine consecutive years and rose by 23 per cent during 2011 alone to $584.70, according to data compiled by Bloomberg.

In reality the average overall production cost is most likely close to double this estimate.

Evy Hambro has demanded that gold companies stop “misleading” investors with their focus on cash costs and come up with new measures that show the total “all-in” costs including capital.

“The worst thing that could possibly happen is if the gold price went up because that would take the pressure off management to take hard decisions,” Hambro said.

According to Bloomberg data, up until around 2005 gold mining companies typically boasted valuations that were more than twice those of other mining companies.

The forward price-earnings (PE) ratio of gold miners was 30 to 35 during 2005/06, compared with less than 15 for world equities.

The situation has now however switched, with gold miners currently at 10 versus around 12 for global equities.

Figure 2: Rising Gold production Costs – Courtesy Thomson Reuters GFMS

Certainly mining company executives are feeling the pressure, with Newmont Mining CEO Richard O’Brien to step down from 1 March next year as the company looks to boost production amid rising costs.

BHP Billiton has also announced that it is looking for a new chief, whilst Anglo American’s CEO Cynthia Carroll stepped down from her position in October.

Newmont is probably one of the best – or worst examples (depending on your perspective) of an under-achieving gold company.

For the first half of this year, Newmont reported attributable gold production of 2.49 million ounces, down from 2.56 million ounces for the same period last year.

Meanwhile, net income of $294 million for the second quarter ($0.59/share) was down massively from $445 million ($0.90/share).

The mining industry cannot afford to be complacent.

Years of strong commodity prices and robust demand have unfortunately encouraged laziness and ineptitude in some instances, whilst also masking poor management decision-making.

At the end of the day shareholders have every right to demand higher returns from a sector that has experienced boom times, yet in many instances has disappointed.

Whether miners will have the intestinal fortitude to concentrate on earnings and returns rather than size, remains to be seen.

Perhaps tough economic circumstances will assist management in reaching the right conclusions, as project funding is increasingly difficult to source and will likely remain so for the foreseeable future.

Perhaps the management of miners will realize that bigger isn’t necessarily better?

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report