Day One Announcements Set Tone for Successful RIU Explorers Conference

THE CONFERENCE CALLER: There were plenty of ASX announcements from companies eager to attract attention of delegates to get things started on Day One of the RIU Explorers Conference.

Global Lithium Resources (ASX: GL1) reported the results of a Scoping Study carried out at the company’s Manna lithium project east of Kalgoorlie in Western Australia.

Global Lithium owns 100 per cent of the Manna lithium project that hosts a Total Mineral Resource Estimate (MRE) of 32.7 million tonnes at 1 per cent lithium oxide (Li2O), with 58 per cent in the Indicated category.

“The results of the Scoping Study show the true quality and real potential of the Manna lithium project,” Global Lithium managing director Ron Mitchell said.

“The exploration team worked extremely hard throughout 2022 to provide a solid foundation for the Manna lithium project.

“The development team will now diligently progress all the necessary technical components and engineering work streams to ensure the project is sufficiently de-risked allowing the company to progress to a final investment decision next year.”

Cygnus Metals (ASX: CY5) announced assay results from the first two drill holes undertaken at the company’s Pontax lithium project in the James Bay region of Québec, Canada.

Results from the first two holes returned multiple intercepts including individual intersections of up to 16.5 metres at 1.1 per cent Li2O that are some of the thickest Cygnus has achieved to date, which it said highlights the scope for growth at Pontax.

“These are very strong results which demonstrate Pontax has both grade and width,” Cygnus Metals managing director David Southam said.

“Given that spodumene has already been outlined over a 700 metres strike length, the results highlight the significant potential for growth through systematic exploration.”

Miramar Resources (ASX: M2R) declared results from analysis of end of hole samples from aircore drilling it believes to have increased the potential for the company’s 100 per cent-owned Whaleshark project to host iron oxide copper gold (IOCG) mineralisation.

End of hole (EOH) samples from the 2022 aircore drilling campaign were analysed for a multi-element suite, including IOCG pathfinders with one hole returning the highest copper and cobalt results Miramar has seen from Whaleshark to date.

“At Whaleshark, we have the right aged rocks, the right style of alteration and the right combination of elements typically associated with IOCG mineralisation,” Miramar Resources executive chairman Allan Kelly said.

“As we continue to explore the project, we see more similarities with the signatures of various large IOCG deposits.”

Ausgold (ASX: AUC) informed punters of initial results from a multi-rig drilling program it commenced in December 2022 at the company’s 100 per cent-owned 2.16 million ounces Katanning gold project (KGP) in Western Australia.

The company received initial program results for reverse circulation (RC) drilling (55 holes for 4,763m) it declared to demonstrate the presence of new high-grade zones of mineralisation along strike from and within the projects’ Central Zone and Southern Zone Resource areas.

“High-grade results from new drilling highlights the strong case for the Katanning gold project to be a much larger project,” Ausgold managing director Matthew Greentree said.

“The 25,000 metres drilling program is testing areas along strike from known Resource areas.

“With the majority of the program still underway, these early results anticipate further discoveries to extend Resource areas and expand targeted opportunities regionally at the Duggan, Stanley and Lake Magenta prospects.”

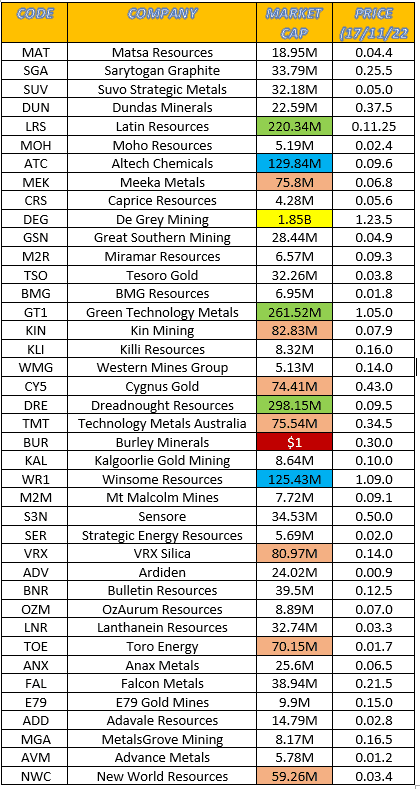

A quick look at the table to our left shows the Resurgence Conference has once again attracted companies that represent investment opportunity across the board.

A quick look at the table to our left shows the Resurgence Conference has once again attracted companies that represent investment opportunity across the board.