Caltex closer to closing Australian refineries

Caltex is a step closer to closing its 70-year old Australian refining businesses.

Caltex Australia (ASX: CTX, Share Price: $12.35, Market Cap: $6.1 Billion) has flagged the closure of its two domestic oil refineries at Kurnell in Sydney and Lytton in Brisbane, threatening 800 jobs and possibly marking the end of its presence as a fuel refiner in Australia after almost 70 years.

The refineries supply around one-third of Australia’s petrol needs.

Caltex has written down the value of the refineries by $1.5 billion (from $1.8 billion to $340 million), partly because of the effect of the strong Australian dollar on its business.

The closures would leave Australia with five remaining operating refineries.

The review of the two refineries is about six months from being completed.

The company says no decision had been made, but that the status quo could not continue.

Caltex Australia said its forecast net operating profit for calendar 2011 was unchanged at between $180 million and $200 million, compared to $302 million in 2010.

The review will also investigate how to improve the refineries’ productivity, including expanding the types of crude that could be processed, thus increasing the range of refined products with commercial uses.

Refineries in countries such as India and Singapore are more modern, sometimes producing more than one million barrels a day and handling a wider array of crude oils, compared to an average 100,000 barrels a day for an Australian refinery.

What you might not know is that Caltex isn’t your typical oil company.

What makes it different from the others is that it doesn’t explore for and produce its own oil, like for example BP or Shell.

These are known as fully-integrated energy companies, with upstream operations (i.e. exploration and production (E&P), as well as downstream operations (refining).

Caltex by comparison is purely a refiner of crude oil that it purchases from its suppliers, which it then processes into different types of fuels.

Caltex is also a retailer, owning service stations right across Australia.

Caltex is an interesting situation to reflect upon for a couple of reasons.

Firstly, its problems are symptomatic of those being faced by most value-added, manufacturing industries in Australia at the present time.

The success of our mining industry has led to a robust Australian Dollar, which in turn is destroying the viability of many other industries.

Rising cost pressures that Caltex and many other businesses are facing are being exacerbated by our strong currency.

Global refiners like Caltex face relatively high input costs, as fuel demand in the United States and Europe remains fragile and cheap supply comes online in Asia.

Caltex’s refining business competes in a regional marketplace, where product can be moved internationally, so the company’s margins are impacted by regional demand and supply dynamics.

Over the past decade, there has been increasing refining capacity built into the Southeast Asian region, particularly in Singapore, where new mega-refineries can produce petrol and other refined fuel products much cheaper than they could possibly be produced here in Australia.

And it’s not just a temporary phenomenon either.

There are structural issues that have made it a tough business to be in for companies like Caltex for some time.

Caltex is one of the biggest refiners in Australia but is competing with Shell on the east coast, which has the benefit of producing its own oil.

Caltex in the future is likely to be just a retailer, running service stations and selling impulse items when you stop to pay for fuel.

They’ll still operate here as a listed company, but domestic refining won’t be part of their picture.

In the meantime, Caltex will most likely concentrate on higher-margin oil products, a strategy that is working well for its marketing unit, which is expected to achieve a record result for 2011.

All of this is a sobering reminder of how important it is to look past the rhetoric typically associated with the petroleum industry.

Governments are always quick to put the boot into oil companies, when in actual fact it’s usually governments that manage to gouge the unsuspecting motorist the most.

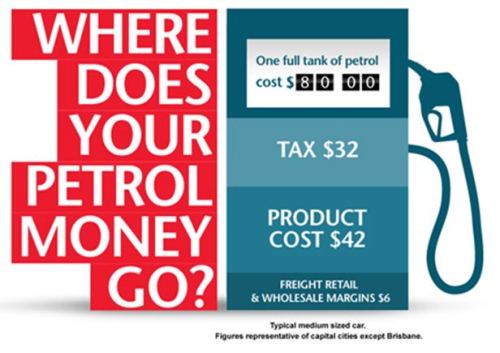

Caltex is a refiner and with most motorists constantly griping about the rising cost of filling their tanks, it’s enlightening to examine exactly how ‘lucrative’ the refining business really is.

I’ve shown this graphic before, but it’s worth taking another look.

It shows exactly where the money goes from a typical tank of petrol, with governments at both state and federal levels taking the lion’s share.

Given the massive cost of establishing and maintaining refining infrastructure, the low returns generated from the business in Australia really make it a mug’s game.

No rational-thinking CEO would enter the business (or continue in the business) given the return on investment now on offer.

Companies like Caltex therefore appear unlikely to have a long-term future in refining in Australia, given the marginal returns on offer.

This opens up discussions on issues like whether it’s strategically necessary for Australia to have refining operations based here, from a security angle for example.

In the event of some sort of military conflict, surely it’s preferable for us to be able to source own petroleum locally, rather than have to rely on international shipments?

This is the scenario potentially facing Australia if both Caltex and Shell decide to throw in the towel on domestic refining.

National security issues should at least be considered in my view.

We’ll know more in about six months time, but the writing is on the wall for another business that’s suffering as a result of the mining boom.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report