Batteries Generating Market Buzz

COMMODITY CAPERS: If you haven’t heard rumblings in recent times regarding the rise of global battery markets, then you really haven’t been paying enough attention.

The world received its first lithium-ion battery in 1980 when it fell off the drawing board of American inventor John Goodenough.

From humble beginnings they went on to take over the world, being responsible for powering so many of the devices we use every day, such as our phones, computers and televisions.

Climate change and carbon emissions have combined to provide the perfect storm for Li-ion batteries thanks to their use in the development of electric vehicles (EVs).

This is by no means a new phenomenon.

In 2017 EVs had become the environmental touchstone and were predicted back then to dominate the market sooner, rather than later, due mainly lower costs for battery manufacturing and commitments from car companies to establish themselves as market leaders.

In its Electric Vehicle Outlook 2017 report, Bloomberg New Energy Finance noted just how quickly EVs would start to dominate the global car market.

“By 2040, 54 per cent of new car sales and 33 per cent of the global car fleet will be electric,” Bloomberg said.

“Falling battery prices will bring price-competitive electric vehicles to all major light-duty vehicle segments before 2030, ushering in a period of strong growth for electric powertrain vehicles.

“While EV sales to 2025 will remain relatively low, we expect an inflection point in adoption between 2025 and 2030, as EVs become economical on an unsubsidized total cost of ownership basis across mass-market vehicle classes.”

That was then and just last year more than 2.6 million electric vehicles were sold in the world’s two emerging major EV markets, with Europe selling almost as many plug-in electric cars as China a trend that is showing no signs of slowing down this year.

Western European plug-in electric car sales rose to 12.3 per cent of car sales in 2020, while in China EV sales hit 5.4 per cent of the broader market in 2020.

Australia should not be left out of any discussion concerning the purchase of electric cars.

If there is a new status symbol in town, Australians, particularly those in the West are always eager to cut in line for their bit of the action.

In its 2021 August/September Horizons members’ magazine the Royal Automobile of Western Australia declared the state to be on the way to 2000 registrations of EVs, with the WA Department of transport data affirming 1819 EVs had been registered by March 2021.

“These included battery electric vehicles (BEV), plug-in hybrid electric vehicles (PHEV) and fuel cell electric vehicles (FCEV),” RACWA said.

“Of these, 1393 were BEV, 411 were PHEV and 15 were FCEV.

“The most common BEV was the Tesla Model 3, at 426, followed by the Nissan Leaf (201) and the Tesla Model S (149).”

Battery market growth creates unique opportunities for Australian producers of key commodities, notably lithium, graphite and cobalt.

“Already, demand for batteries and associated technologies has changed the game for producers of lithium, cobalt and graphite, turning them into outliers at a time when other commodities are undergoing price falls and declining investment,” the Department of Industry, Science, Energy and Resources said.

“Time and technological change will show whether the battery boom can drive wider change in global markets and energy models.

“Investment is being drawn by the promise of electric vehicles, and by the potential for community-generated solar power to displace grid monopolies and fossil fuels.

“This investor interest is, in turn, generating sizeable funds dedicated to further research and development.

“Commodity demand will be strong in the short term, but long-term prospects for battery technology are still in motion.

“The potential opportunities are vast, and investment and production decisions of today could cast a long shadow into the future.”

Australia ranks fourth globally for lithium deposits and is currently the largest producer of lithium.

Source: DISER: Resources and Energy Quarterly June 2021

The country hosts substantial resources of spodumene, potentially making it a major producer over the longer term.

Graphite is used for a range of products, including lubricants, foundry operations, brake linings, and steelmaking, with the use of graphite in batteries on the rise.

China is currently the main producer of graphite, but there is noise from countries such as Brazil and Turkey that they too could host greater reserves than what is presently known.

Australia’s reserves of graphite are comparatively modest, and at this stage there are no operating graphite mining projects, however, a range of projects are currently being progressed.

Refined cobalt supply is expected to fall below consumption, which is being pushed up by demand from Li-ion batteries and aerospace industries and advancements are suggesting developing battery technologies may require less cobalt.

Until that time cobalt will need to be found somewhere, and again China leads the refined cobalt producer pack, owning 70 per cent of global refinery capacity.

What is advantageous to potential Australia producers is that the bulk of cobalt is sourced from mines in the Democratic Republic of Congo, where there is increasing concern over the use of child labour and environmental damage.

Australia has significant cobalt reserves, although there are no dedicated cobalt mines in operation with most cobalt mined as a by-product of copper, gold or nickel mining.

Around 40 of Australia’s gold and nickel operations are co-located with some form of cobalt deposit.

If you think this is all going unnoticed by the country’s mining industry, think again

At the 30th Diggers & Dealers Mining Forum in Kalgoorlie this year, there was any number of companies more than willing to talk up their battery metals credentials that are combining to contribute to a revolutionary transformation of the traditional nature of the mining sector.

One such company was IGO Limited (ASX: IGO), which concluded the forum by taking out the prestigious Dealer of the Year Award at the closing night Gala Dinner.

Speaking during his presentation spot on Day One, IGO managing director and chief executive officer Peter Bradford went through the company’s recent transition from a diversified producer seven years ago with two profitable but short-life base metals mines and a 30 per cent minority stake in the Tropicana gold mine (with international partner AngloGold Ashanti) to one specifically focused on metals that are critical to a green energy world.

The movement began with IGO’s acquisition of the Nova nickel-copper project in WA through a friendly takeover of Sirius Resources in 2015.

As Nova reached commercial production, the company then known as Independence Group saw crystal ball opportunities of the emerging demand for battery metals to drive a global trend towards clean energy.

A subsequent change of tack that included the sale of its Tropicana stake to Regis Resources, resulted in IGO holding a unique portfolio of nickel, copper, lithium and cobalt assets in a Tier 1 jurisdiction and further exploration projects focused on discovery of the next generation of nickel and copper mines.

Bradford said the company’s impetus was its belief in a green energy future, “and our belief that we can make a contribution to a better planet.”

COVIC-19 didn’t succeed in driving the climate change conversation away, but it did ramp it up.

“COVID hit the pause button on the planet, we paused power production, we paused industry and we paused transportation,” Bradford said.

“As a result, we all got an opportunity to see what could be. Places around the world that haven’t seen clean air for generations were able to see clear blue skies.

“That’s allowed all of us to visualise what could be possible and how we could make a contribution for future generations.

“Our strategy is to be a globally significant supplier of clean energy metals and a diverse suite of products made safely, ethically, sustainably and reliably.

“To my knowledge, we are the only company globally that produces that one-stop for electric vehicle battery metals.”

Source: IGO Diggers & Dealers Presentation

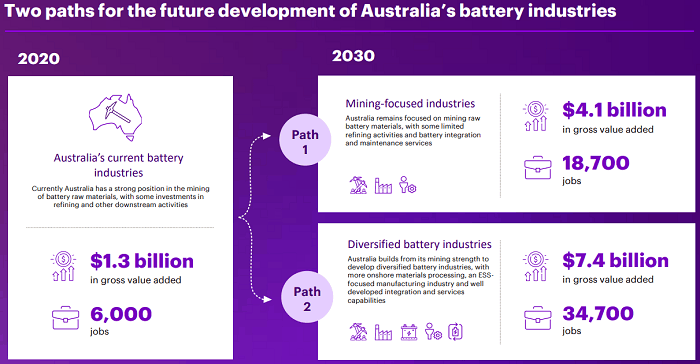

Batteries are now the tip of the global manufacturing iceberg.

A report prepared in June this year for the Future Battery Industries Cooperative Research Centre (FBICRC) by Accenture determined that diversified battery industries could contribute $7.4 billion annually to Australia’s economy and support 34,700 jobs by 2030.

The report concluded that Australia now has a major economic opportunity to leverage its competitive advantages to become a dominant supplier of battery minerals and expand its role within a growing global industry.

“This report provides a compelling business case for Australia to develop into a competitive player in the international batteries industry, and Australia has many strengths for succeeding in this ambition,” Stedman Ellis, CEO of the FBICRC said.

“We are shining a light on the different segments of an industry in which Australia can be a leader, and there is substantial economic value to gain if we capture the opportunity.”

The report lays down a pathway for Australia over the next ten years, during which time the opportunity exists for real industry growth, shaped by changing international relationships and driven by technological improvements in batteries, increasing demand for energy storage and regulatory changes to energy systems.

Source: Accenture – Future Charge: Building Australia’s Battery Industries Report

Demand for batteries has grown steadily but is now forecast to accelerate, increasing nine to ten-fold over the next decade, with sales expected to reach US$133-151 billion by 2030.

I think we would all like a piece of that.