An industry under siege: why we need the junior resources sector.

MARK GORDON: So, why do we need the junior resources sector?

Speaking from a purely selfish viewpoint I need it so I can keep working in a sector that I have a strong passion for.

The mineral exploration and financial sectors involved with resources have given me a fantastic career over 24 years – one that I wouldn’t have changed, despite some frustrations over the years!

It is a sector that has been under siege of late from a number of quarters, which unfortunately has the effect of scaring investors away.

The first and key issue is the market, which we can’t do much about. This is a nature of the beast – markets are cyclical, with junior resources being more volatile than most, and given the risk profile it is one of the first sectors to suffer when funds dry up.

We have just been through the extraordinary ‘Super-Cycle’, driven by an ever emergent China, but unfortunately this has been interrupted by the GFC and ongoing headwinds, inhibiting broad growth in the global economy.

However, we are now back into an overall flat tracking to gently down trending and volatile period, following a dramatic downturn in the sector from March 2011 until June 2013.

Funding is still out there; however the market is much more discerning about where it goes than it was during the boom.

We have also been increasingly under siege from other interests – some sections of the media and noisy vested interest and anti-mining groups amongst others.

Although everyone is entitled to their ‘opinion’, it seems to me that a lot of the commentary that comes out of these groups is ill-considered, uninformed and emotive.

This actually often seems to be targeted – note the ‘shut the gate’ campaigns against coal and coal seam gas in New South Wales, and the anti-coal sentiment starting to come out in a number of quarters – this has been reinforced by Government decisions against compliant DA’s for a number of proposed Hunter Valley coal operations, the cancellation of several CSG leases and more recently all licence applications.

Fortunately, the large majority of Australians remain overall supportive of mining, and understand that it is an essential part of Australia’s economy.

A recent case that caused a storm in the media was the ANU’s decision to divest itself of seven resource stocks, based on a review of the university’s portfolio commissioned under the university’s Socially Responsible Investment Policy, and provided by CAER.

I am not going to go into detailed commentary on this issue here, however one point should be raised – although the media and commentariat picked up on the ‘move away from fossil fuel’ tone of associated comments by the Vice-Chancellor, only two of these companies are in fact involved in fossil fuel production!

The companies that were divested from the portfolio include:

Iluka Resources (ASX: ILU) – mineral sands – 1998 merger;

Sirius Resources (ASX: SIR) – nickel/copper – Recapitalisation of Croesus Mining – relisted 2008;

Sandfire Resources (ASX: SFR) – copper/gold – 2004 IPO;

Independence Group (ASX: IGO) – nickel/gold – 2000 IPO;

Oil Search (ASX: OSH) – 1929 – Oil and Gas Incorporated (PNG);

Santos Petroleum (ASX: STO) – Oil and Gas – Incorporated 1954; and

Newcrest Mining (ASX: NCM) – gold/copper – 1990 merger.

All are successful, Australian listed companies, with at least four (without knowing the detailed history of Oil Search) starting life as junior explorers that subsequently made large discoveries.

Herein lies a key reason why we need junior explorers:

Firstly, THEY MAKE DISCOVERIES, and are a vital part of the mineral resource sector in Australia.

Instead of being denigrated, maybe they should be lauded and held up as positive examples of what we can achieve here in Australia?

Whilst we must engage with the community and alleviate their concerns I will stress that it seems the industry is under siege from many quarters.

Secondly, and most importantly, mining is a key part of Australia’s economy.

However, some anti-mining groups use the argument that mining contributes a relative small amount to Australian GDP (around 10%), and employs a relatively low number of people (i.e. we are productive!).

On the GDP side they often forget the proportion of GDP in the mining related industries, which takes the total mining sector contribution to approx. 20 per cent, a very significant part of Australia’s economy.

More importantly, mining is a key contributor to national income through exports of mineral resources.

This cannot be stressed enough – at the current time, if mining should stop, Australia would lose close to 60 per cent of its foreign income; imagine your household losing at least 60 per cent of its income (which is what has occurred in the households of a number of mining professionals).

Published figures (see graph below from 2012 – 2013) show the contribution of mineral resources to Australia’s exports – note this includes bulk commodities, with the significant rise from 2005 largely due to increases in volume for iron ore and coal.

.jpg)

Source: Minerals Council of Australia

However, pre-2005 minerals exports were still a significant part of our export industry, averaging around 35 per cent of export earnings in the preceding 30 years.

Given recent price falls in iron ore and coal we would expect to see the overall resources contribution fall, however as history tells us it will and should remain a vital contributor to Australia’s income.

Of the resources exports, approximately 20 per cent by value are non-bulk commodities, including base and precious metals.

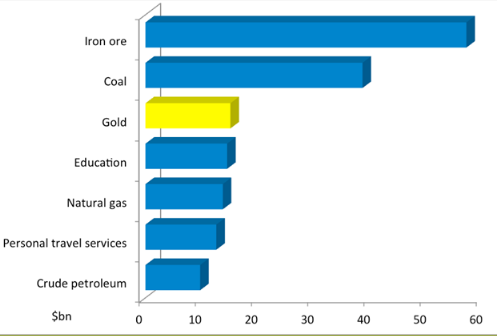

Gold is Australia’s third single largest export after iron ore and coal – the value of Australia’s seven largest exports are shown below – note that out of these five are natural resources and two are services, reinforcing the importance of natural resources to Australia’s wealth.

Australia’s seven largest exports – 2012-2013. Source: Minerals Council of Australia

Junior explorers are an important part of this, making approximately 66 per cent of the non-bulk discoveries in the period 2004 to 2013, and 50 per cent of the same in the period 1994 to 2003.

Mark Gordon

Senior Resource Analyst

This article first appeared in ![]()