THE BOURSE WHISPERER: Graphex Mining (ASX: GPX) released an announcement to the ASX relating to the company’s ‘markets first’ strategy as it develops its Chilalo graphite project in south-east Tanzania.

Graphex Mining highlighted its recent efforts in developing and enhancing its ‘markets first’ strategy, with a strong focus on non-Chinese markets to complement the company’s existing customer relationships in China.

A key development in this strategy has been the advancement of a low-risk, low capital-intensive, value-added products strategy to enhance the value of its concentrate sales to be included in the upcoming definitive feasibility study (DFS).

What caught our eye, however, was the company’s analysis of the graphite market and the inherent differences within that most punters are probably not, but should be, aware of.

Below is pretty much a word-for-word lift from the company’s ASX announcement.

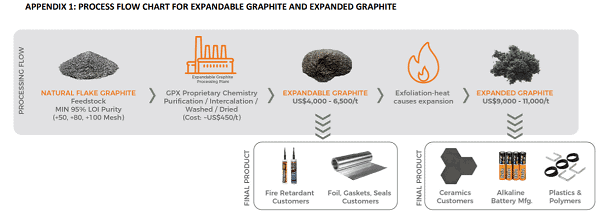

EXPANDABLE GRAPHITE

Over the past four years, Graphex has engaged numerous end users as well as three independent laboratories to evaluate the use of Chilalo flake graphite (in various mesh sizes) for the production of expandable graphite and to determine how Graphex expandable graphite would perform when compared to other expandable graphite producers and products.

Evaluations have consistently concluded that Chilalo flake graphite, using two different intercalation / oxidation compound formulas, meets the performance characteristics for graphite foils and fire-retardants.

Due to its unique chemistry markers, Chilalo flake graphite meets critical parameters that are required for fire-retardant manufacturers.

Sales of natural flake graphite into value-added markets will achieve higher prices than selling the same graphite into applications such as refractories which generally don’t require any performance qualifications other than meeting minimum purity requirements.

Refractories can formulate to any flake graphite signature in the world to ensure a consistent supply of natural graphite.

This is another reason why reference to ‘graphite prices’ is irrelevant without further defining other characteristics, even if, for example, it is the same product (ie. a +895 product, which is +80 mesh, 95 per cent loss on ignition (LOI), will sell for a higher price as a fire-retardant pre-cursor material than it would selling to a refractory manufacturer).

Source: Company announcement

MICRONISED GRAPHITE

Micronised graphite is a processed form of natural or synthetic graphite, produced by fine grinding flake graphite concentrate into specific micron particle size distributions.

This process allows smaller mesh sizes (- 100 mesh or -200 mesh) to be used as raw material feedstock, creating a high potential margin for producers.

The key requirements of micronised graphite are achieving a range of micron particle size distributions (PSD) and PSD axis variances to meet the various specifications and performance metrics for targeted applications.

There are multiple applications which use micronised graphite products including lubricants, dispersions, pencil, friction, carbon brush, automotive seals, industrial polymers, and Hot Metal Forming (HMF).

The strategy to pursue micronised graphite has a number of advantages:

• Natural flake graphite feedstock to produce micronised graphite is -100 mesh, 95 per cent LOI, which is also a graphite product competing with Chinese suppliers and Syrah Resources Limited and is therefore more likely to attract low prices;

• Micronisation equipment is relatively low capital cost (even so, it is proposed as a second phase following commissioning of the main Chilalo plant); and

• Significant value uplift achievable (weighted average sales price for standard purity micronised graphite based on Graphex’s targeted product mix increased to US$2,800/t FOB Port compared with significantly lower prices for selling -100 mesh concentrate into China).

COARSE VS FINE FLAKE GRAPHITE – A TALE OF TWO MARKETS

Graphite is unlike mainstream commodities in that independent market information is scarce and prices are set between the buyer and seller, rather than by reference to an index or exchange.

There is also no single price that applies to all graphite, with the graphite market comprising a multitude of different applications and specifications.

Furthermore, pricing is impacted by many factors outside of purely flake size and purity.

Coal companies will be quick to point out the differences between coking coal and thermal coal given the different uses and resultant pricing.

Thermal coal is used to generate electricity and currently sells for approximately US$50-65/t depending on quality, while metallurgical or coking coal is used to make steel and currently sells for approximately US$150/t.

The differences in uses, supply/demand and hence pricing are even more pronounced between coarse and fine flake graphite and it is therefore critical to distinguish between these two categories rather than simply talking about ‘graphite’ as a single market.

The table below shows several key differences between coarse and fine flake graphite.

Source: Company announcement

Source: Company announcement

Graphex believes that the major difference comes down to supply and notes that separating Table 1 into coarse flake and fine flake only is an oversimplification due to the complexities of specifications, applications and markets within each category however it broadly demonstrates the substantially different dynamics impacting each size category.

Since the initial discovery of Chilalo in 2014, Graphex has worked to develop its understanding of end markets while seeking to partner with strategic investors to enable delivery of the project.

The Chilalo project is underpinned by a high proportion of large flake material with expansion characteristics, which has taken the company down the expandable graphite market road due to expandable graphite’s attractive growth and value characteristics as well as the size and growth expectations of the expandable graphite market applications, the premium prices for large flake graphite in general and the suitability of Chilalo graphite for the production of expandable graphite applications.

This has resulted in Graphex prioritising supplying the expandable graphite market as its primary focus.

Email: info@graphexmining.com.au

Web: www.graphexmining.com.au