Market Movements Encourage Brownfield and Greenfield Explorers

COMMODITY CAPERS: The renewed optimism for the resources sector is built on the resurgence of interest in brownfield expansions and exploration of greenfield projects.

The Department of Industry, Innovation and Science, in its Resources and Energy Quarterly for December 2017, informs us that the mining industry has continued to account for a decent share of Australia’s overall economic growth in 2017.

The mining industry’s main concern is that the government bean counters place it in the same basket as the oil and gas sector, which does make it difficult to get a reliable reading on mining’s current standing.

Investment in oil and gas took a big hit last year, which DIIS suggests – when coupled with declining export values – could see the mining industry make a smaller contribution to overall economic activity in the coming two years.

“Steel production cuts in China have placed downward pressure on the price of Australia’s biggest export — iron ore — in the December quarter,” DIIS chief economist Mark Cully said in the report.

“Continued moderation in Chinese steel production, coupled with increased supplies from both Australia and Brazil, are expected to weigh further on iron ore prices over the next two years.

“The outlook for base metals prices are generally more optimistic than for iron ore and coal (although mixed across the individual commodities).

“Strong growth in global industrial production — particularly the manufacturing of stainless steel, vehicles and aluminium-based packaging — and infrastructure development, particularly in China, has boosted demand.”

Minelife founder, and old friend of The Roadhouse Gavin Wendt, recently noted that commodities prices moved higher by just under eight per cent during 2017.

This considered the performances of all the various sectors – including precious metals, base metals, energy, grains, soft commodities and animal proteins.

However, it was the drop in agricultural prices that dragged down the composite returns as many industrial commodities prices soared.

“When looking at the performance of the commodities sector as an asset class during 2017, many industrial commodities that are the building blocks of infrastructure around the world outperformed the major equity indices,” Wendt said.

“For example, the price of palladium – both an industrial and precious metal – appreciated more than 56 per cent over the course of the year.

“In addition, aluminium and copper both posted better than 30 per cent gains, whilst zinc, nickel and lead were all up more than 20 per cent on the year.

“As 2018 is upon us, I believe there are strong prospects for a continuation of a broad-based commodities rally.”

Of course, where it all begins is on the ground with exploration the first step in any long march towards mining project development.

Exploration is more than just throwing a dart at a map and saying, ‘let’s see what’s there’, it is an educated decision based upon gained knowledge about the location, type, quantity and quality of deposits, which helps to inform future development.

This means explorers need consider a range of factors to ensure the outcomes of their exploration activities exceed the costs involved.

Judgements need to be made in terms of include initial and long-term land access agreements, current and predicted commodity prices, regulatory environments, geological prospects, and tax and royalty arrangements.

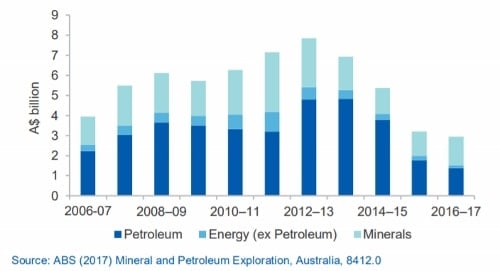

The Western Australia, Department of Mines, Industry Regulation and Safety (DMIRS) tells us that Australia’s mineral exploration expenditure was $1.6 billion in 2016–17, up from $1.4 billion in 2015–16.

“Western Australia contributed over $1 billion of this spend with the gold and iron ore sectors attracting the largest share,” DMIRS said.

“Gold exploration expenditure in Western Australia increased significantly from $385.9 million in 2015–16 to $509.5 million in 2016-17.

“Iron ore exploration also increased (but only marginally to) $281.6 million.”

As well as WA exploration appears to be going, DIIS reckons the nation is lagging in terms of overall exploration expenditure.

Australian exploration expenditure fell by eight per cent in 2016–17 to $2.9 billion with the pesky petroleum industry emerging as the main culprit with its exploration expenditure decreasing by 23 per cent to $1.4 billion.

Minerals exploration managed to offset this marginally with a rise of 10 per cent in 2016–17 to $1.6 billion.

The increase in minerals exploration was largely driven by nickel, cobalt, and gold, all of which were credited to favourable movements in commodity prices.

“After five consecutive years of declines since 2012, exploration expenditure on iron ore has stabilised, remaining unchanged from 2015–16 levels of $291 million,” DIIS said.

“Growing global supply and expectations of low prices have discouraged a rebound in exploration activity.”

In 2016–17, Australian resources sector mineral exploration expenditure targeting new and existing deposits increased by 17 and 7 per cent, to $0.5 and $1.1 billion, respectively.

The positive movement in market conditions encouraged exploration at new deposits.

Greenfield exploration was also on the rise as mineral deposits not previously drilled – or known to exist – suddenly coming into vogue as commodity prices increased.

The old standard of commodities, gold, featured high in exploration expenditure, increasing by 26 per cent in 2016–17 to $689 million — accounting for 44 per cent of Australia’s total minerals exploration expenditure during the fiscal year.

Gold exploration activity was stimulated by higher world gold prices and a lower AUD/USD exchange rate, which improved the profit margins of Australian gold producers.

Base metals exploration expenditure rose by 17 per cent in 2016–17 to $271 million, again riding a wave of higher commodity prices, producing the first yearly improvement since low prices triggered a steady decline back in 2012.

Australia’s copper exploration expenditure was driven by an improved outlook for copper prices and was one area to enjoy the rise in battery metal interest and increased by 5 per cent, to $136 million — accounting for 50 per cent of Australia’s total base metals exploration expenditure.

The battery metal curiosity surrounding cobalt dragged nickel along for the ride with exploration expenditure for both also recording a strong rise in 2016–17, up by 59 per cent to $81 million.

Nickel prices also enjoyed more traditional support following stronger than expected demand growth in China, which is seeking to increase its output of stainless steel.

Other base metals recorded a rebound in exploration activity in 2016–17 resulting in an increase in exploration expenditure on zinc, lead and silver by 10 per cent, to $55 million.