Killi Resources Encounters Tanami Gold Mineralisation

THE DRILL SERGEANT: Killi Resources (ASX: KLI) reported the first round of drilling results from aircore and diamond drill programs completed at the company’s West Tanami project in the Kimberley of Western Australia.

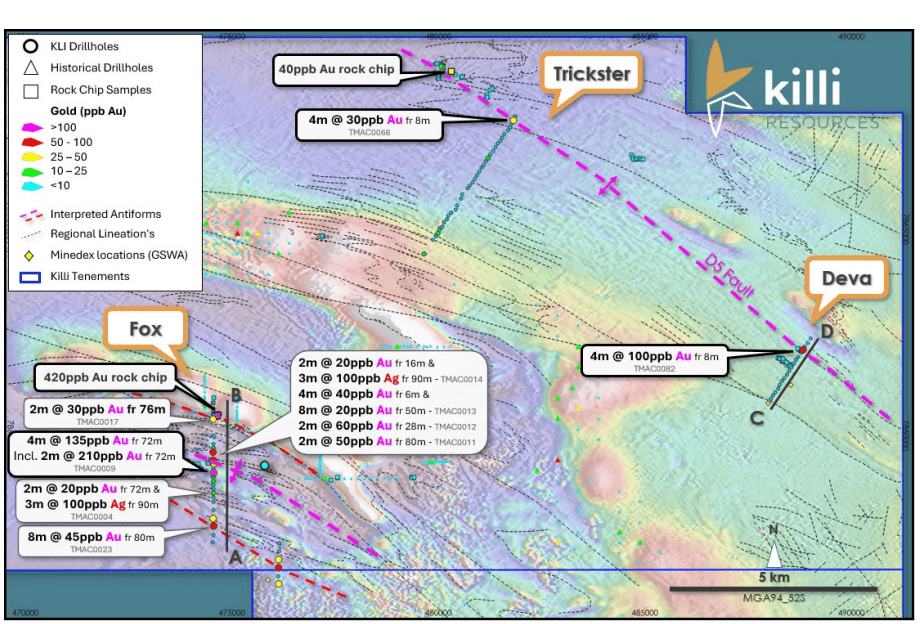

Killi Resources said results returned from the Fox prospect identified a 2.8 kilometre wide corridor anomalous for gold, silver and arsenic, aligning with the company’s model for a sediment-hosted gold system, and similar to those already found in the Tanami.

Multiple intercepts of anomalous gold, arsenic and silver were intersected at the Fox prospect, with all elements aligning with the geochemical fingerprint for a sediment hosted gold system.

The highest result returned was 4 metres at 135ppb gold from 72m, located at the interpreted hinge zone.

Two regional aircore lines were completed at the Trickster and Deva prospects consisting of 54 holes, which are the first drilling to be carried out over this newly identified prospective gold structure the company believes could represent the main mineralising feature from the Tanami district.

A result was returned at the eastern end of the southern line of 4m at 100ppb gold from 8m depth, in bedrock below alluvial cover.

“These results are exactly what we are looking for, and in the right rocks, as these low-level gold and arsenic anomalies are indicative of orogenic sediment-hosted gold systems throughout the Tanami,” Killi Resources CEO Kathryn Cutler said in the company’s ASX announcement.

“Callie was found on a 50ppb gold and arsenic result, so we are thrilled to have +100ppb gold intervals and to have identified the Dead Bullock sediments on our ground.

“These are the first two pieces of the puzzle, so we can now narrow in on the structures to find those fold hinges we need as the gold traps.”

TO READ THE FULL ANNOUNCEMENT: CLICK HERE

Web: www.killi.com.au