What the Brokers Say

WHAT THE BROKERS SAY: Stockbroking firm, Bell Potter runs its eye over the Pilbara iron ore industry and its main players.

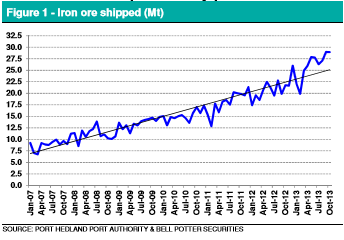

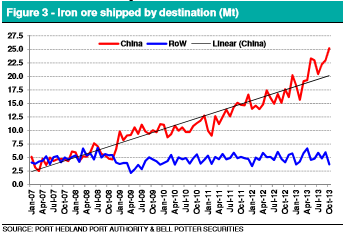

Iron ore sector Port Hedland – October 2013 – Total iron ore shipments flat, record shipments to China.

Bell Potter has dissected the Port Hedland Port Authority’s October 2013 monthly statistics. Key points to arise from the data are:

– Total iron ore shipments were above trend at 28.9 million tonnes (Mt) (flat Month on Month (MoM), up 33 per cent Year on Year (YoY)); and

– Iron ore shipments to China were 25.2Mt (up 10 per cent MoM, up 43 per cent YoY).

According to Bell Potter production capacity expansions from BHP Billiton and Fortescue Metals Group contributed to the increase in China shipments over October 13.

Spot pricing holding up; upside risk to consensus pricing

Spot iron ore prices (62 per cent CFR) are currently ~US$136/t, holding up despite record iron ore exports to China. With the financial year to date iron ore price averaging ~US$133/t, Bell Potter said it envisages upside risk to FY14 average consensus price estimates (i.e. ~US$115-120/t).

Prices will have to average ~US$105-110/t from now until 30 June 2014, to meet average consensus estimates.

Bell Potter nominated Fortescue Metals Group (ASX: FMG) and BC Iron (ASX: BCI) as its preferred iron ore exposures

FMG’s production growth and declining unit cost profile are unique in the industry. With expansion capex winding down, FMG’s free cash flow will improve markedly into FY14. FMG’s next focus will be to de-gear its balance sheet; pay dividends; potentially increase production to 175 to 180 million tonnes per annum (Mtpa); and reduce unit costs.

BCI is the cleanest leverage to iron ore prices, and is a lower cost producer (BP est ~A$48/t) compared to its junior peers. With a strong balance sheet (net cash of A$68 million), Bell Potter sees potential for BCI to:

1) Pursue small-scale growth opportunities; and

2) Return excess free cash flow to shareholders.

Atlas Iron (ASX: AGO) is a higher cost producer compared with BCI and FMG, and its FY14-15 CAPEX commitments are substantial ($464 million for Horizon 1 to take production from 10Mtpa to 14 to 15Mtpa).

The company’s earnings and valuation are therefore more leveraged to iron ore prices than its peers.

AGO is Bell Potter’s least preferred iron ore exposure due to expected weak earnings and free cash flow over FY14/15.

AGO is expensive on short term earnings (FY14 P/E 12x; and FY15 P/E of 8x). AGO’s expansion beyond 12 to 15Mtpa (Horizon 1) will require third party infrastructure agreements and significant capital.

Bell Potter company analysis

Atlas Iron Ltd (ASX: AGO)

AGO is an independent Australian iron ore company, mining and exporting Direct Shipping Ore (DSO) from its operations in the Northern Pilbara region of Western Australia.

The company’s business model has been to develop iron ore resources close to road infrastructure, avoiding the need for significant investment in rail infrastructure.

Horizon 1 expansion:

AGO is aiming to increase production capacity to 10Mtpa by the September 2013 quarter and 12Mtpa by the June 2014 quarter from the incremental addition of the Mt Dove, Abydos and Mt Webber mines. Surge capacity could see Horizon 1 volumes reach 15Mtpa.

Horizon 2 expansion:

Longer term AGO plans to utilise 46Mtpa of port capacity at Port Hedland through the development of its S.E. Pilbara assets. The Horizon 2 expansion will require a rail solution.

We recognise upside earnings risk should iron ore prices remain elevated or from positive sentiment should AGO strike an infrastructure deal for Horizon 2. However, AGO is most leveraged should iron ore prices correct (as we expect).

In addition, a Horizon 2 deal will only further delay positive free cash flow. We are also concerned that Horizon 2 would bring online relatively high cost production (compared with existing production) in a weaker iron ore market.

BC Iron Ltd (ASX: BCI)

BC Iron (BCI) is an iron ore producer with key assets in the Pilbara, Western Australia.

The company’s core focus is the Nullagine iron ore project, an unincorporated 75 per cent:25 per cent joint venture with FMG.

The Nullagine Joint Venture is currently producing DSO at a rate of 6Mtpa (BCI equity per cent 4.5Mtpa). The NJV uses Fortescue’s infrastructure at Christmas Creek to rail ore to Port Hedland for shipping.

BCI remains our top pick in the junior iron ore sector. With minimal CAPEX to spend going forward and cash costs in the bottom half of the cost curve, we see BCI generating substantial free cash flow over the short- to medium-term.

We think it’s likely that a large proportion of this free cash flow will be returned via higher dividends.

Valuation upside exists through its project inventory work, and we are expecting significant earnings and cash flow growth in FY2014.

Fortescue Metals Group Ltd (FMG)

FMG is an independent iron ore producer in the Pilbara region of Western Australia.

The company is currently producing iron ore at rates of around 120Mtpa. By the end of 2013, FMG aim to be producing at 155Mtpa rates.

There is also potential for expansions beyond 155Mtpa rates, through the development of resources close to its existing infrastructure, or through the development of a third production hub.

However, to achieve such production growth, additional port capacity would need to be secured.

FMG’s production growth and declining unit cost profile are unique in the industry. With expansion capex winding down, FMG’s free cash flow will improve markedly into FY14.

FMG’s next focus will be to de-gear its balance sheet; pay dividends; potentially increase production to 175 to 180Mtpa; and reduce unit costs.

Disclaimer: The above is intended as a guide only. The Roadhouse accepts no responsibility for investments made from this advice, successful or otherwise.