Gold once again in the spotlight

GAVIN WENDT: Over the past fortnight or so, the price of gold has declined to levels around its $1,600 long-term trend-line, which we’ve previously spoken about.

What’s most bemused me about gold’s recent decline (and all previous sell-offs during its 12-year bull run), has been the economic rhetoric accompanying it.

Quite simply, it seems to have boiled down to economic complacency. It is argued that share markets are recovering (well some of them superficially anyhow), growth is reappearing (in some sporadic circumstances) and investors are feeling more comfortable about their economic outlook (in some instances). Therefore the argument goes, there’s no logical reason to own gold.

Nothing could be further from the truth. Sharemarkets are rising (notably in the US) because of the trillions of dollars that have been pumped into the market since the GFC, through various forms of quantitative easing (QE) and money-printing.

Naturally, if you keep pumping enough air into a balloon, the balloon must eventually swell in size.

The problem with the US economic balloon is that it’s also full of holes.

Cheap credit (via record low interest rates) has provided the mechanism with which the US economic balloon has been inflated – not just since the GFC – but for the past 20 years or more since sound economic management went out the window.

Cheap interest rates led of course to both a consumer and property boom unparalleled in US history, allowing average Americans an over-inflated sense of their own economic wellbeing.

The debt binge would eventually end – and it did so with the implosion of the US economic balloon during the GFC in 2008.

Now the US is applying exactly the same economic remedy that caused the mess in the first place – more easy credit and low interest rates (and this time around a devalued currency) in order to get Americans to spend once more. But it’s inevitable it will fail.

The scary part is that the average American’s lot has not improved despite the trillions poured into the monetary system – in fact, by virtually all measures (net income, purchasing power and investment returns) – they’ve going backwards.

According to US statistical group, TrimTabs, their tracking of real-time wages and salaries shows that the US has in fact entered into a recession this year.

This of course contradicts official Government statistics, but what the data shows is that after-tax wages and salaries net of inflation have been shrinking since the second week in January.

What has been growing dramatically in real time this year is income and employment tax payments. Before inflation, after-tax wages and salaries have grown by just 0.3 per cent.

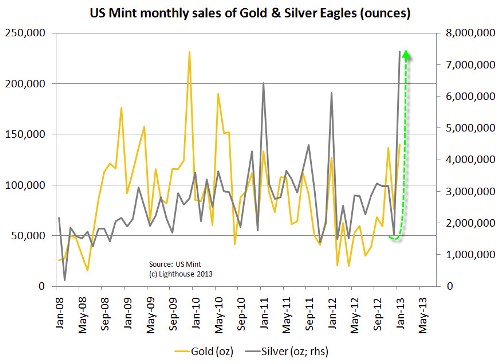

The average American is actually buying more gold, which demonstrates that the economic outlook as far as they are concerned is clouded to say the least. Figures from the US mint show that gold coin demand for February was up more almost 300 per cent on the same period in 2012. Gold coins are the ultimate form or insurance for ordinary investors.

Sales of American Eagle gold coins totaled 80,500 ounces during February, a rise of 283.3 per cent from the same month last year, while sales of the same line of silver coins more than doubled from a year earlier to nearly 3.4 million ounces.

Excluding figures for January, February 2013 saw the second-highest monthly gold coins sales by the US Mint since September 2011, the month that saw gold set an all-time high above $1900 an ounce.

Since then, only November last year has seen more American Eagle gold coins sold by the US Mint, when 136,500 ounces were sold.

And it’s the same story with respect to silver coins. After smashing their all-time monthly sales record during January with 7.5 million Silver Eagles sold (even with production halted for half the month), silver eagle sales have continued at a record-setting pace.

The Mint’s February sales statistics indicate record sales of 3.37 million silver eagles for the month, eclipsing February 2011′s previous February record of 3.24 million ounces sold.

In contrast with gold coin sales, gold exchange traded funds (ETFs) saw their biggest combined monthly bullion outflow on record. What this indicates is that whilst the big boys are chasing higher speculative returns elsewhere, ordinary investors are increasingly demanding the security and peace of mind that only gold can deliver.

And it’s not just the mums-and-dads that are buying gold in record volumes – so too are central banks.

In fact, the actions of central banks worldwide continue to fly in the face of the hordes of financial experts that point to an improving economic picture and renewed confidence.

During 2012 central bank gold buying reached its highest level since 1964, rising by 17 per cent to 534.6 tonnes, with 145 tonnes purchased during Q4 2012 – up 9 per cent from the same period a year ago and the eighth consecutive quarter in which central banks were net purchasers of gold.

What this situation clearly demonstrates is a clear lack of confidence on the part of emerging economies in the traditional and established world reserve currencies – like the dollar, the euro and the pound.

And who could blame them, given the trillions of dollars that have been printed and fed into the financial system for little net effect?

As experienced precious metals commentator David Levenstein best described it this past week, “There is a huge dislocation between the physical market of gold and the paper market for gold. But, unfortunately, at the moment, it seems that speculative trades are determining the trend, much like the tail wagging the dog.”

Whilst the price of gold has fallen in the short-term, I share his view that the decline does not reflect the very real fundamentals that include a European, US and Japanese debt crisis, global currency wars and the real risk of recessions. And as we’ve previously highlighted, when sustained economic recovery does eventually take place, surging interest rates and inflation will be the result.

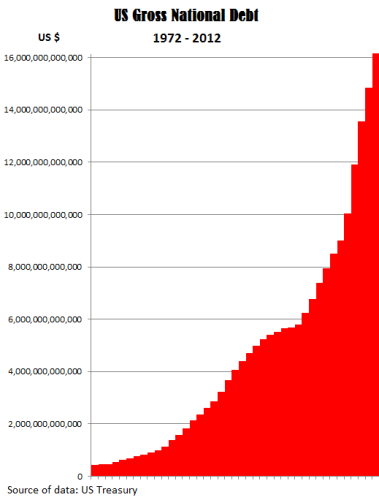

As Levenstein highlighted last week, since 2008 the official net public debt of the US federal government has increased by $5.5 trillion – which is more than double the size of the total net public debt of the US in 2007 when it was $5 trillion.

The total net debt of the US government has exploded to more than $11 trillion, or roughly 80 per cent of GDP.

Over the same period, the US Federal Reserve has more than tripled the size of its balance sheet to around $3 trillion through a series of bond buying programs.

Despite the trillions in bail-outs and stimulus spending, the US economy is in most respects stagnant and the unemployment rate remains close to 8 per cent.

And the situation in Europe is dire and getting worse – contrary to the opinion of many commentators.

In fact the Eurozone economy is likely to shrink for the second consecutive year, with countries like France and Spain missing fiscal targets.

Olli Rehn, the European commissioner for economic and monetary affairs, forecast growth across the 27 nation European Union of just 0.1 per cent this year and a contraction of 0.3 per cent among the 17 countries in the euro zone.

Levenstein says it best: “While the mainstream media is reporting an economic turnaround, I am not convinced. And, as Federal Reserve Chairman Ben Bernanke is trying to create the illusion of wealth by pumping money into the system, the average US citizen is having a tougher and tougher time as the cost of living is higher relative to their salaries. Furthermore, the economy is not growing and unemployment remains elevated.”

As noted gold-watcher Barry Stuppler opined this past week, “Many of the financial commentators on CNBC and CNN expressed their opinion that the twelve year track record of gains for the gold price was over”, for the following reasons:

Investors are switching out of gold into stocks for growth and income;

There is no inflation, and investors have no reason for owning gold;

The US economy is recovering, easing pressure for more monetary stimulus;

Investors like George Soros are reducing their core holdings of gold; and

World demand for physical gold dropped 4 per cent in 2012.

The same arguments against gold have been made many times over the past 12 years – most notably during 2006 and 2008.

The experts of course proved to be wrong, with gold quickly recovering and hitting fresh highs. And I have no doubt that the current situation isn’t any different.

It’s been reported within China that central bankers there have a three-phase, 10-year route map to make the yuan a full reserve currency and gold will be a central part of their strategy.

This contrasts with most Western central banks over the past three decades, which have effectively tried to get rid of gold from the international monetary system.

What we witness now are the dollar, euro and yen in crisis.

The sensible investor understands that gold’s recent price drop does not alter the long-term picture. I remain bullish on gold and believe that after a period of consolidation around its long-term support line at US$1,600, it will inevitably push higher.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report