2012 – A tough year for investors and explorers

If you weren’t invested in CSL Limited (ASX: CSL), The Commonwealth Bank, (ASX: CBA), Telstra (ASX: TLS) and/or Sirius Resources (ASX: SIR) it’s been a pretty tough old year in the investment community.

CSL is up 66.25 per cent, Telstra is up 30.3 per cent, and CBA is up 23.75 per cent.

These three stocks would have also given their shareholders dividend yields of: 6.8 per cent for CBA if you bought at the start of the year; 8.4 per cent for Telstra; and CSL would have given you 2.6 per cent for the year.

These yields were for the purchaser if they bought these stocks on January 2nd, 2012.

The bonus would have been the imputation credits that you were entitled to from Telstra and CBA.

In Resources Land, the standout performer was undoubtedly Sirius Resources.

On 25 July 2012 the stock closed at 5.7 cents, it is now trading around $2.

Capital appreciation for this is 3510 per cent.

Now to coin a phrase from a much advertised credit card commercial, that is priceless.

It can happen, but in resource exploration it’s very unlikely.

For every Sandfire Resources (ASX: SFR), Sirius or Western Areas (ASX: WSA), there are hundreds of companies that don’t strike it rich.

Additionally, with regards to Sirius and Sandfire the drill campaigns were the last roll of the dice in those respective areas.

In Sirius’ case, the Nova deposit was discovered at the back end of $20million exploration spend in the Fraser Range.

Both discoveries have ignited areas that had been considered in the past, but not necessarily for the mineral that was actually discovered.

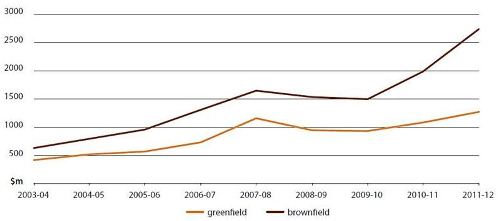

According to the Bureau of Resources and Energy Economics (BREE), expenditure on mineral exploration activities increased in recent years, however, it is a spend which has not been equally distributed between Greenfield and Brownfield sites.

Greenfield Vs Brownfiled exploration spend 2003-04 to 2011-12. Source: BREE

For those unfamiliar with the vernacular, Greenfield sites are areas that have been subjected to minimal exploration activity, if any, while Brownfield sites usually have operating mines in the region with supporting infrastructure and exploration activity is generally undertaken in an effort to identify additional resources.

BREE statistics for the past two years indicate most of the growth in exploration expenditure has been at Brownfield sites with Brownfield exploration expenditure in 2011–12 totalling $2.8 billion, an increase of 38 per cent from 2010–11 (in 2012–13 prices).

Over the same period, Greenfield exploration expenditure increased 17 per cent to $1.3 billion.

Exploration is a tough gig, and many more people have lost money looking for minerals than have found them.

That job is made even more difficult when the current governments have no empathy for minerals exploration, and their first consideration is to tax the industry instead of helping it.

There is no doubt an exploration rebate is long overdue for Australian exploration companies, akin to the Canadian system.

The numbers crunched by BREE show the average cost per metre drilled at Greenfield and Brownfield sites have converged over the last eight years and are now at similar levels.

Cost per metre drilled 2003-04 to 2011-12 (2012-13 Australian dollars). Source: BREE

The Bureau puts this down to the cost of Greenfield exploration increasing faster than the cost of Brownfield exploration.

While this may have led to a rise in exploration activity due to the cost per metre drilled for the two types of exploration having been relatively similar, it has also resulted in Brownfield exploration, in terms of both metres drilled and expenditure, growing at a substantially higher rate.

“The different growth rates in exploration metres drilled, particularly since the Global Financial Crisis in 2008–09, indicate the tendency of mining and exploration companies to focus on Brownfield sites,” BREE said.

“In part, this is because Brownfield sites typically have a lower development cost compared to Greenfield developments.”

It’s obvious to everyone in the real world that mining helped Australia avoid a recession twice recently, and without encouragement for new discoveries, the mining industry has been looking at other municipalities for future investment.

This is particularly the case for the smaller sector.

Truth be told, a lot of Aussie exploration companies would like to explore in their back yard, but the current impediments make it more likely that they will head offshore.

The history of the exploration success via Mark Creasy, Graeme Hutton and Lang Hancock may just be that if exploration companies and prospectors are not given further incentives to help find the next Nova.

The big companies are the lifeblood of the mining industry, as they are the ones that still spend when the market gets tough.

But smaller companies are generally pushing the proverbial uphill with regards to exploration spend, and they have only one source of funding.

This funding dries up when the going gets tough, and tax deductions for investors would make that funding easier.

Peter Hayes

Investment Manager

![]()