Richard Beazley – Peak Resources

The Roadhouse was paid a visit by rare earth exploration play Peak Resources managing director Richard Beazley.

Peak Resources listed in November 2006, was that on the back of the Ngualla rare earths project?

No. When Peak listed the then Board was focused on a number of gold exploration leases in Australia.

When current non-executive chairman Alistair Hunter joined the business he contributed some gold leases located in Tanzania. That was pivotal in the sense it put Peak Resources into East Africa.

The next pivotal Board decision was to broaden our exploration for phosphates – which brings us to where we are today.

So Ngualla was originally a phosphate target. Why the change of focus from gold to phosphate?

It was the opportunity for phosphate development in the country and supplying phosphates into the African space for fertilisers, and into India as well, potentially.

Rare earths really are a new frontier aren’t they? If you will excuse the pun, they really are breaking new ground in the mining industry.

It’s an emerging market. They’ve been used for a while in specific applications.

Now they’re being brought forward because our technologies demand those applications be used in products we use every day.

The rare earths at Ngualla have become Peak’s major focus now?

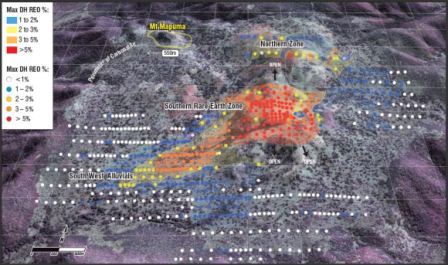

What we have in the centre of the project area is an area rich in rare earth oxides.

The discovery of which came about when drilling for phosphate?

Correct. On the outer rim of the project is the phosphate, where we commenced drilling.

During the program, two holes were drilled in to the central area and two holes in the northern area of the project.

These returned assay results that demonstrated the value for the rare earths at Ngualla as potentially 200 times more than the value for the phosphates.

On that basis we decided to change the drilling program around to the centre of the project where the rare earths are situated.

What do you now know about your, what is now, rare earths play?

We have identified three different mineralised zones that have given us a resource of 170 million tonnes.

That is a significant number as it places Ngualla as the fifth largest rare earths project in the world, outside of China.

The rare earth market is nominally 120 to 130 thousand tonnes of rare earths per annum.

This is 170 million tonnes grading well above the norm. This represents potentially many centuries of mining.

Commercially, where we are developing is in the weathered high-grade zone known as the Southern Rare Earth Zone, which provides more ‘returns’ for ore above our cut-off grade of three per cent.

We have 40 million tonnes over four per cent.

There are a number of companies within the rare earth space at the moment, many with resources that may be economical, but nowhere near as substantial as the reserves you appear to have?

That’s right.

So what advantages does Peak Resources have over its competitors?

Firstly in terms of tonnes, we have mine life. There are a lot of mines with ‘tonnes’ so we can tick that off, but that doesn’t really cull the pack all that much.

Our important advantage is grade. As in all mines, it’s all about tonnes and grade and grade is king as they say, so when I compare our grades to those within our peer group – we have 170Mt for around 4Mt of contained rare earth oxides.

There are some other projects with very high grades but they generally have very low tonnages.

This is a rare earth project, which means it’s not a typical gold mine or base metals play.

We’re dealing with 15 elements, not just one or two, which complicates the picture somewhat.

That’s a lot of elements for one project. How do you know which will deliver the best value?

We need to understand the marketability of those elements – what it means in terms of price, as one rare earth element has different pricing to the others.

They range in price from tens of dollars per kilogram to several thousand dollars per kilogram.

We need to understand that. For us value is very important when we look at the mix of elements we have got in our ground. To understand value in a closed market we need to engage with targeted customers and negotiate positions.

Have your recent studies enabled to you focuses on which of the 15 elements present are the ones for you to concentrate on?

Yes. The ones that have value are those for which there will be an under-supply that will increase in price due to that situation and that we have significant supply.

Thus our attention will be on neodymium for the magnet market and europium for the phosphor markets around the globe.

The cerium market is predicted to be in over-supply and there will be downward pressure on price.

Having said that, there’s always the view that part of that over-supply will be taken up by new products as the metal, has been to date, relatively unavailable for new product development.

For instance, Molycorp, in the United States, has developed a new water absorbing product that uses cerium.

Now that is a product outside the current market space. Molycorp’s anticipates all its cerium production will be funnelled into this new product.

That means the quantity of cerium coming out of that mine will not impact the current market, so the impact on price will be lessened, hopefully maintained at current levels.

Is that why people may have trouble understanding the rare earths market? They hear about rare earth companies yet they don’t know about rare earths and how they are really used. There is a certain mystique surrounding them.

Non-technically minded people get them confused with a whole raft of other elements like lithium and graphite that overlap in products like batteries, which causes some confusion.

The other issue I’ve found after travelling through the UK, North America, and Australasia is, particularly with the Australian market, investors see time to be a major issue.

When we look at the development time at Mt Weld, or Arafura and Alkane – you’re talking decades to bring the product to market, which just add to the uncertainty and risk.

Our project is a bit different in that we have an ore body that is cleaner, in a relative sense; it’s simpler because we essentially have low levels of acid-consuming minerals, no deleterious minerals, effectively background levels of uranium and thorium and no other economic minerals to complicate the metallurgy.

That’s important from a processing point of view. The chemistry is simpler and removes potential complications in the metallurgy downstream that our competitors have to expend cash and time to reslove.

You have low levels of uranium and thorium. Why does that add and not subtract to the project value?

We virtually have no uranium or thorium – just background levels – so that is not going to cause any issues with processing and limits problems from a cost point of view for processing, handling, storage, and transport.

Importantly, there are no other economic minerals in our rare earths. That means our metallurgy solution is far simpler. We don’t have to extract other minerals apart from the rare earths.

So would you describe Ngualla as a ‘simple’ rare earths project?

I would use the word relatively in there as well. If I just say it is simple people might think it’s like a gold mine, it ain’t like a gold mine.

The rare earth business is far more complicated.

I would say – in a relative sense to other rare earth projects, Ngualla is ‘simpler’.