Iron Ore: keeping things in perspective

Iron ore continues to be in the news in a major way.

There are arguments and counter-arguments with respect to the near to medium-term price outlook, with varying degrees of optimism and scepticism.

If you read some of the reports about in the financial press you could be forgiven for thinking that the iron ore industry must be in the midst of a catastrophic crisis, with prices plumbing all-time lows as demand plummets and supply surges.

The reality, once one looks past the dramatic headlines accompanying recent developments, is vastly different.

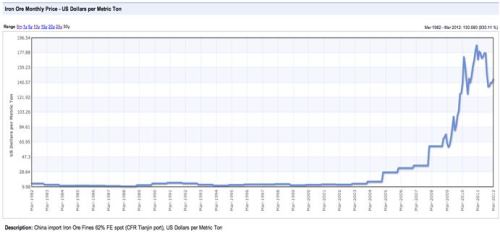

The chart below puts everything into perspective. Whilst the iron ore price has retreated from its pre-GFC peak, it is still trading at a price that’s almost seven times higher than the $20 per tonne price that it averaged for more than two decades between 1980 and 2004.

This provides an enormous margin for iron ore players, particularly when compared to the margins that the industry had become accustomed to during the course of the preceding decades.

BHP, Rio and Fortescue

From a local perspective, Rio Tinto (ASX: RIO), BHP Billiton (ASX: BHP) and Fortescue Metals Group (ASX: FMG) – the world’s second, third and fourth biggest iron ore miners behind Brazil’s Vale – plan to add a combined 235 million tonnes of new mine capacity by 2015, nearly equal to Rio’s total output in 2012.

In terms of the outlook for demand, Rio Tinto forecasts steel demand will grow by about 3 per cent a year for the next decade, which is well down on 10 per cent growth rates during 2009 – 2011, but in my view reflective of a more realistic and sustainable demand scenario.

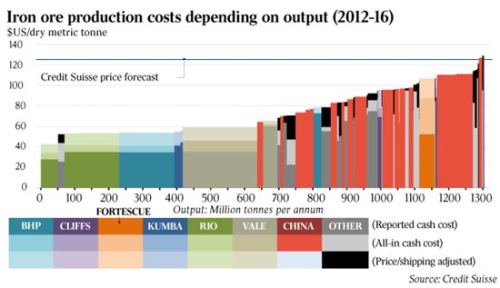

Rio Tinto, which derives more than two-thirds of its revenue from iron ore, is counting on its premium ore and low operating costs to provide hefty profit margins despite any cyclical downturn in the iron ore market. Rio’s economies-of-scale allow it to mine iron ore at a lower production cost than anyone else in the iron ore business, as the chart below demonstrates.

What’s also significant is how much iron ore production would be wiped out at an iron ore price of $80/t or lower – much of it Chinese.

The iron ore business has typically been dominated for decades by three major players – Rio, BHP and Vale – which together have accounted at one stage for as much as 80 per cent of the world’s seaborne iron ore trade.

And there’s a simple reason for this – iron ore is a bulk commodity, which means it’s typically a low-margin business, where the stuff has to be dug and moved in enormous volumes in order to generate a reasonable profit.

Being a bulk commodity, infrastructure costs are huge, with returns generated over a lengthy period of time.

The fundamental characteristics of the iron ore business – high capex/ low-margins/large volumes/massive funding requirements/medium to long-term pay-back – are not features that typically attract smaller players into the industry.

As a result, iron ore is predominantly the domain of mining heavyweights that can utilise their sizeable balance sheets to minimize exposure to potentially crippling debt levels.

Chinese Production a Major Factor

Falling grades and volatile prices are making life difficult for China’s iron ore miners and threatening to push them out of business.

It is estimated that as much as 40 per cent of China’s more-than-a-thousand iron ore producers shuttered production during the course of 2012 when iron ore prices slumped.

China’s mostly small-scale miners produce around a third of the raw material for the country’s steel industry.

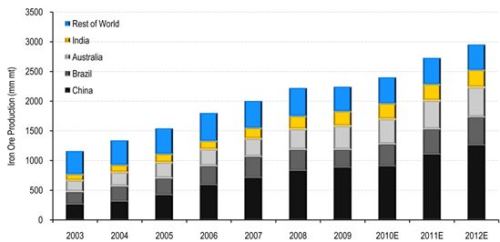

The chart below highlights exactly how big an iron ore producer China is, which is probably a surprise to many.

China is typically a swing producer and its mines rely on strong iron ore pricing above $120 in order to remain viable.

However, despite the critical role their output plays in determining China’s need for imports, the fragmented nature of the industry makes it difficult to estimate how deeply the miners were hit when iron ore prices fell to three-year lows below $87 a ton during September 2012.

Any future price weakness will once again place significant pressure on China’s iron ore producers.

Pricing Outlook

Iron ore will always tend to be a relatively low-margin business. The ultra-high pricing environment of the past decade, which encouraged smaller hopefuls into the sector, is in no way typical.

Prices will eventually level-off and begin to recede as supply catches up with demand. However as we highlighted earlier, iron ore prices are around seven times higher than their average over the preceding two decades – and are unlikely to retreat back to these former levels.

The key from my perspective is how much supply effectively becomes uneconomic if the iron ore price falls below $80/t.

Indeed, let’s cast our minds back to the latter stages of 2011 and 2012, when iron ore prices fell below $100/t to see the panic that was generated in iron ore markets.

The one thing we can be sure of is volatility, with the bulk of iron ore sales based on the volatile spot market, rather than the certainty of an annual fixed price as had been the case for decades.

The iron price hit a 16-month high of $158.90/t on February 20 this year, but has since dipped to be currently trading around $110/t.

The production cost for the smaller Chinese miners is around $100 – $120/t, about three times more than the major producers in Australia and Brazil.

With respect to BHP and RIO’s Pilbara production expansions, the new capacity is aimed at meeting demand surges and minimizing the strong price spikes that can be disruptive to the industry.

In many instances the larger producers have touted major capacity expansions that have eventually translated into production on timeframes markedly longer than initial estimates.

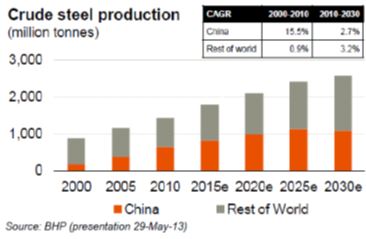

A BHP presentation on 29 May forecasts China’s steel production to peak in about 2025 at about 1.1 billion tonnes per annum. Steel production growth is forecast to moderate as steel intensity per unit of GDP declines.

The market consensus view is firmly of the opinion that iron ore is easing in price and may have further to fall, as Chinese steel mills run down inventory before restocking.

Both Morgan Stanley and Macquarie believe this to be the case and have published similar reports over the past fortnight. They believe iron ore prices will weaken further over the coming months (from current seven-month lows around $110/t), before rebounding during H2 2013.

This is no great surprise, as it is merely a reflection of typical annual Chinese buying habits.

As the annual summer holiday season approaches, China’s steel mills typically run down inventories as production levels decline. They then look to take advantage of the low iron ore price environment to replenish inventories.

The move over the past few years away from annual contract pricing and towards spot pricing has resulted in a correspondingly higher level of price volatility, which accentuates underlying price movements.

Pressure on Fortescue

The problem for Fortescue is that circumstances are to a large degree beyond its control. Its future is solely dependent on the maintenance of strong iron ore prices. It’s a one-commodity company, without the earnings diversification of BHP and RIO.

Exacerbating the problem is the fact that FMG has taken on massive debt levels to compete with BHP and Rio Tinto in terms of size and scale. Unfortunately, they operate better assets, produce product at a much lower cost and are in a much sounder financial position.

Fortescue was initially fostered and supported by the Chinese in a similar fashion to the way the Japanese during the 1970s fostered and financed many Australian coking coal producers in order to try and break the market dominance of the key coal industry players, with the aim of sourcing cheaper product.

Whilst Chinese and Indian steel producers have been vocal supporters of independent iron ore players like Fortescue, which have the potential to break the market dominance of the sector leaders, they won’t pay a higher price to purchase iron ore.

Steel producers are going through enormously tough times and will accordingly purchase the lowest-cost product available.

BHP and RIO’s lower-cost operations and hence capacity to operate in a lower-price environment puts tremendous pressure on FMG position over the medium to longer-term.

Summary

I believe prices will average around $125 per ton during 2013, with prices easing further during the course of H2 2013, before recovering on restocking during late 2013. For 2014 I anticipate prices will average around $115 per ton, which will still provide robust margins for the major iron ore producers; albeit not as lucrative as pre-GFC levels.

Gavin Wendt is the founder of MineLife, publisher of the MineLife Weekly Resource Report